How to Conduct Stock Audits

By

By

Stock audits sound routine on paper. In practice, they are one of the most misunderstood and poorly executed control exercises across industries.

Whether it is a manufacturing plant, a retail chain, a pharma distributor, an EPC contractor, or an e-commerce warehouse, inventory discrepancies remain one of the largest silent risks on the balance sheet. Not because companies do not track stock — but because they overestimate how accurate their records actually are.

A stock audit, when done properly, is not about ticking boxes or matching numbers. It is about verifying reality.

This guide explains how stock audits are actually conducted on the ground, what works, what fails, and how businesses across industries should approach them without disrupting operations.

What Is a Stock Audit (In Practical Terms)?

A stock audit is the independent verification of physical inventory and its reconciliation with accounting records, ERP data, and supporting documents.

In real life, this involves:

- Physically checking stock quantities

- Assessing condition, usability, and obsolescence

- Verifying ownership and location

- Identifying mismatches between books and reality

- Understanding why mismatches occur

It applies equally to:

- Raw materials

- Work-in-progress (WIP)

- Finished goods

- Trading stock

- High-value spares and consumables

Why Stock Audits Matter Across All Industries

Stock audits are not industry-specific. The risk profile changes, but the problem remains the same.

Common drivers across sectors:

- Inventory used as bank collateral

- Statutory audit and financial reporting

- GST and indirect tax scrutiny

- Internal control failures

- Shrinkage, theft, or pilferage

- ERP data reliability concerns

Industry experience shows that inventory is often the largest current asset — and the least verified.

- Check Out: Stock Audit Services in Delhi

How Accurate Are Inventory Records in Reality?

Industry research consistently highlights uncomfortable truths:

- Manual inventory systems typically achieve 60–65% accuracy

- Barcode-based systems improve accuracy to 85–90%

- RFID-enabled environments can reach 99%+ accuracy, but only when processes are disciplined

Even in system-driven environments, process lapses, not technology, cause most variances.

This is why physical verification remains non-negotiable.

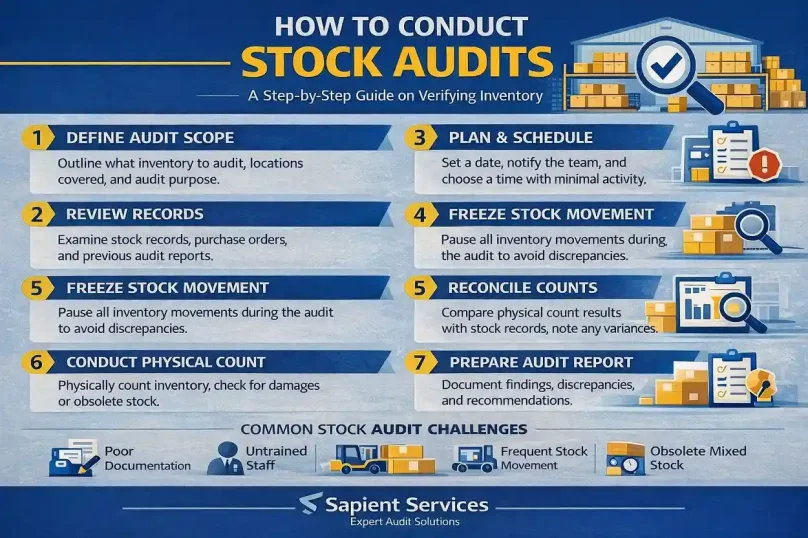

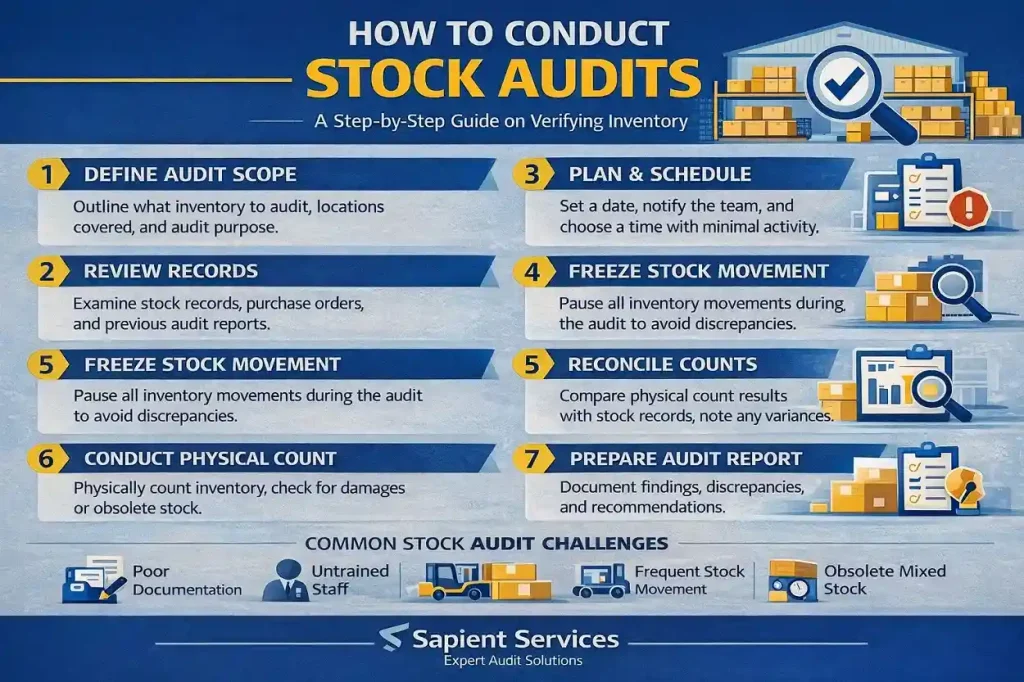

Step-by-Step Process to Conduct a Stock Audit

Step 1: Define the Audit Scope Clearly (Before Anything Else)

This step is frequently rushed — and that’s where problems begin.

Define upfront:

- Which locations are covered

- Which categories of stock are included

- Cut-off date and time

- Purpose (statutory, lender, internal control, due diligence)

A lender-mandated audit will look very different from an internal operational audit.

Mistake to avoid: Trying to audit everything at once without prioritization.

Step 2: Understand the Inventory Flow

Before touching physical stock, auditors review:

- Procurement process

- Storage methods

- Issue and dispatch controls

- Return handling

- Scrap and obsolescence policy

This context matters. Without it, variances make no sense.

Example:

- A manufacturing unit with uncontrolled shop-floor issues will almost always show WIP mismatches.

- A retail chain with poor inter-store transfers will show location mismatches.

Step 3: Review Stock Records and Systems

Records typically examined:

- ERP inventory reports

- Stock registers

- GRNs and issue slips

- Purchase and sales invoices

- Job work and consignment records

At this stage, auditors do not correct numbers.

They assess whether records are capable of being accurate.

Red flags include:

- Negative stock balances

- Manual overrides

- Back-dated entries

- No segregation of duties

Step 4: Freeze Inventory Movement (Wherever Possible)

This is one of the most operationally sensitive steps.

Best practice:

- Pause inward and outward movement during counts

- Use cut-off controls for unavoidable movements

- Clearly mark “counted” and “not counted” areas

In high-volume operations, complete freeze may not be possible. In such cases, cut-off reconciliation becomes critical.

Step 5: Choose the Right Physical Verification Method

Not all stock needs to be counted the same way.

| Method | Suitable For | Practical Reality |

|---|---|---|

| Full physical count | Small warehouses, annual audits | Disruptive but thorough |

| Cycle counting | Large warehouses | Requires discipline |

| Sample-based checks | High-value items | Needs risk-based selection |

| Technology-assisted | Barcode / RFID setups | Depends on data hygiene |

Auditors often combine methods rather than rely on one.

Step 6: Conduct Physical Stock Verification

This is where theory meets the warehouse floor.

Auditors:

- Physically count items

- Check condition and usability

- Identify slow-moving or obsolete stock

- Tag damaged or expired items

- Verify labeling and storage practices

Common real-world challenges:

- Mixed or unlabelled stock

- Incorrect units of measurement

- Old stock mixed with current batches

- Vendor-owned or customer-owned goods stored together

This step requires patience, not speed.

Step 7: Reconcile Physical Stock with Records

Post-count reconciliation identifies:

- Shortages

- Excess stock

- Location mismatches

- Classification errors

Not all variances are losses.

Typical causes include:

- Timing differences

- Incorrect UOM conversions

- System posting delays

- Documentation gaps

The goal is to explain, not just report, variances.

Step 8: Investigate Material Variances

Auditors dig deeper into:

- Repetitive discrepancies

- High-value mismatches

- Items used as loan security

- Controlled or regulated inventory

This often reveals:

- Weak internal controls

- Process shortcuts

- Training gaps

- Poor segregation of duties

These insights are more valuable than the variance number itself.

Step 9: Prepare the Stock Audit Report

A good stock audit report does not overwhelm with data.

It focuses on:

- Key observations

- Material discrepancies

- Control weaknesses

- Practical recommendations

- Risk implications

This is where experienced firms like Sapient Services differentiate — translating warehouse-level findings into decision-relevant insights for management and lenders.

Industry-Specific Challenges (Across the Board)

| Industry Type | Common Stock Audit Issues |

|---|---|

| Manufacturing | WIP valuation, scrap accounting |

| Retail | Shrinkage, inter-store transfers |

| FMCG | Expiry, batch tracking |

| Pharma | Regulatory compliance, cold storage |

| EPC / Infra | Site-wise material tracking |

| E-commerce | Returns and reverse logistics |

Stock audits expose process weaknesses, not just stock errors.

What Stock Audits Cannot Do (Reality Check)

Stock audits:

- Do not prevent theft automatically

- Do not fix poor inventory planning

- Do not replace strong internal controls

- Do not predict demand or sales

They are a diagnostic tool, not a cure.

When Should Businesses Conduct Stock Audits?

Beyond annual audits, stock audits are advisable:

- Before large funding or restructuring

- During ERP migrations

- After mergers or acquisitions

- When inventory turns deteriorate

- When lenders demand independent verification

Banks increasingly rely on third-party audits, and firms like Sapient Services are often engaged for this reason.

Cost vs Benefit: Is a Stock Audit Worth It?

Short answer: usually, yes.

Hidden benefits include:

- Reduced working capital blockage

- Improved lender confidence

- Better demand planning

- Fewer audit qualifications

- Stronger internal controls

Many businesses discover that audit costs are far lower than the value of issues uncovered.

Frequently Asked Questions (FAQs)

1. Is a stock audit mandatory for all businesses?

No. But it becomes mandatory under lender agreements, statutory audits, or regulatory requirements.

2. How long does a stock audit take?

Anywhere from one day to several weeks, depending on size, locations, and complexity.

3. Can stock audits be done without stopping operations?

Yes, with cut-off controls and phased verification, though risks increase.

4. Who should conduct a stock audit?

Independent professionals with audit and industry experience — not internal store staff.

5. How often should stock audits be conducted?

Annually at minimum; quarterly or cycle counts for high-risk environments.

6. Are ERP systems sufficient without physical audits?

No. Systems reflect entries, not physical reality.

7. What documents are required for a stock audit?

Stock registers, invoices, GRNs, issue slips, and location-wise records.

8. How are obsolete or damaged stocks treated?

They must be identified, valued appropriately, and disclosed separately.

9. Can stock audits detect fraud?

They can indicate red flags, but are not forensic investigations.

10. Do lenders rely on stock audit reports?

Yes. Especially when inventory is hypothecated or pledged.