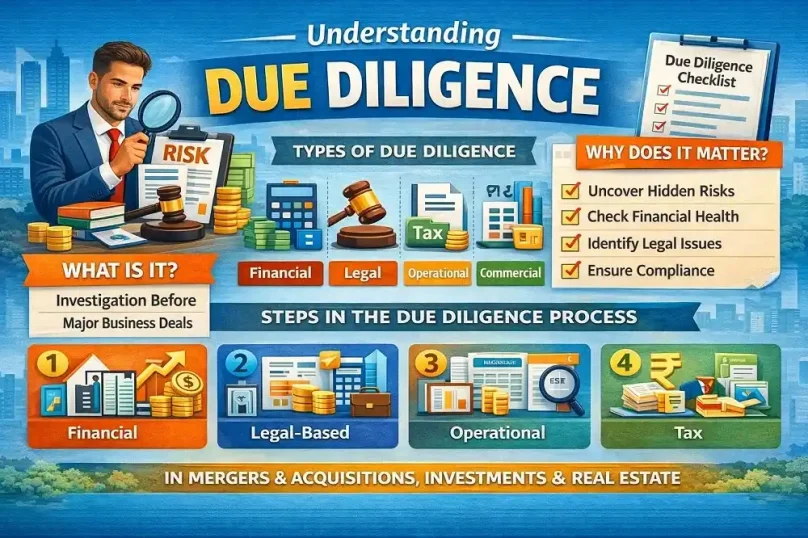

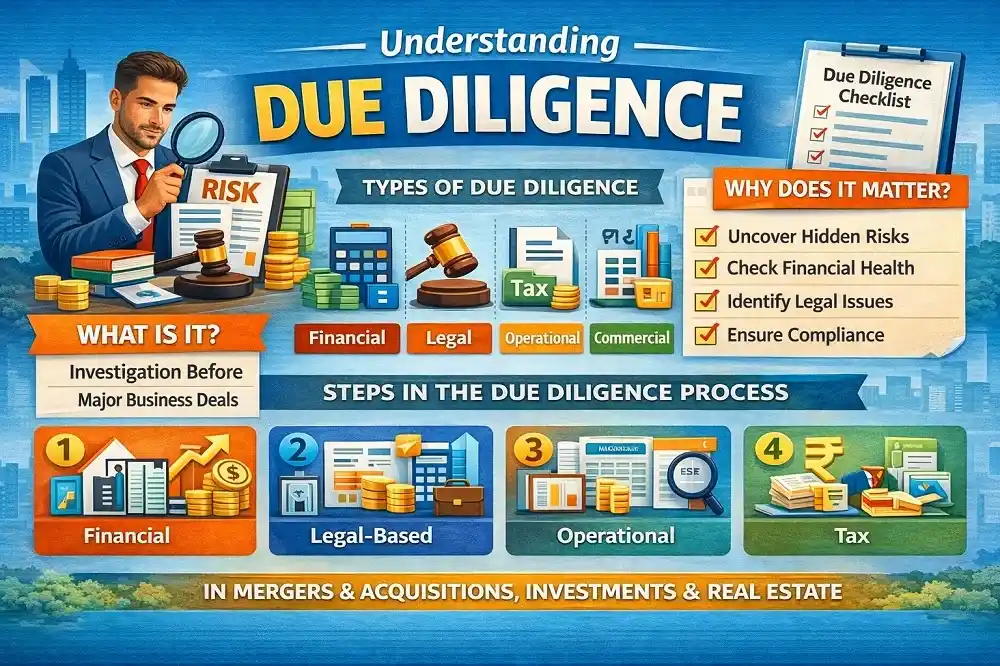

What Is Due Diligence? Meaning, Types, Process & Checklist

By

By

You have found a business worth acquiring, or a deal that looks promising. The financials look clean. The seller is confident. Your instinct says yes. Now what? This is exactly where due diligence begins — and where most deals are either saved or quietly doomed.

Due diligence is the structured investigation you conduct before committing to any significant business transaction. It verifies what you have been told, uncovers what you have not been told, and gives you the information you need to negotiate, restructure, or walk away with confidence.

India’s M&A market crossed USD 123.8 billion in deal value in 2025 — an 18% rise from USD 106.3 billion in 2024. In that environment, skipping proper investigation is not a time-saving shortcut. It is a capital risk you are taking on knowingly — often with consequences that surface only after the deal closes.

Whether you are a promoter planning a cross-border acquisition, a bank evaluating project finance, an NCLT-appointed Resolution Professional working under IBC 2016, or a startup founder receiving your first institutional investor — due diligence is the process that separates informed decisions from expensive assumptions.

|

Need due diligence support for an upcoming transaction? |

Quick Overview: What Is Due Diligence?Due diligence is the process of independently verifying all material facts about a business, asset, or transaction before committing to it. In India, it covers financial records, legal compliance, operational health, tax obligations, IP ownership, and regulatory standing — across the Companies Act 2013, FEMA, SEBI, IBC 2016, and applicable sector regulators. Who conducts it: The buyer or investor, assisted by Chartered Accountants, lawyers, IBBI-registered valuers, and technical specialists. |

Key Takeaways✔ India’s M&A deal value reached USD 123.8 billion in 2025 (EY India M&A Report) — proper diligence is the difference between transactions that create value and those that destroy it |

What Is Due Diligence? — Definition, Legal Basis, and Indian Context

Due diligence is the systematic investigation of a business, asset, or counterparty conducted to verify facts, assess risk, and support informed decision-making before entering a binding commitment. The legal origin is straightforward: it refers to the degree of care a reasonable person must exercise before entering a contract or transaction.

In India’s regulatory framework, due diligence is not merely good practice — it is often a legal requirement. Section 247 of the Companies Act 2013 mandates IBBI-registered valuers for share swap ratio determination in NCLT-approved merger schemes. SEBI’s Takeover Code (Regulation 26) requires an independent due diligence report before an open offer is launched. Under IBC 2016, resolution applicants must verify the financial and operational position of the corporate debtor before submitting resolution plans to the Committee of Creditors.

Beyond compliance, due diligence answers the most important question in any transaction: is what I am being told actually true? The answer to that question — backed by evidence, not assurances — is what separates well-structured deals from costly regrets.

Who Needs Due Diligence — and What Happens If You Skip It?

Due diligence is not reserved for large corporates and investment banks. Every major financial commitment — at any scale — benefits from proper investigation. Here is who needs it most in India:

| Stakeholder | Why Due Diligence Is Critical |

|---|---|

| Banks & NBFCs approving project finance | Verify promoter credentials, asset existence, techno-economic viability (TEV), and repayment capacity before loan disbursement |

| NCLT-appointed Resolution Professionals (IBC 2016) | Verify asset values, operational viability, and resolution plan feasibility before recommending to the Committee of Creditors |

| Private equity & venture capital investors | Validate the business model, financial history, cap table, and IP ownership before committing institutional capital |

| Acquirers in M&A transactions | Uncover hidden liabilities, change-of-control provisions, and regulatory compliance gaps before SPA execution |

| Exporters applying for EPCG / DGFT licences | Verify export obligation fulfillment, chartered engineer certification, and customs compliance before filing |

| SEBI-regulated entities in takeovers | Mandatory diligence report required before open offer launch under Regulation 26 of the Takeover Code |

| Real estate developers & infrastructure buyers | Title verification, encumbrance checks, environmental approvals, and land use compliance before investment |

What happens if you skip it? The answer depends on what you missed. In a 2025 Indian mid-market case reviewed by Sapient Services, an acquirer discovered 18 months post-closing that a key manufacturing facility was operating on a lease with a strict change-of-control clause — a clause that had already been triggered by the acquisition. The landlord was not obligated to renew. The facility had to be vacated. The buyer had just paid for a plant it no longer had the right to use.

This is not an unusual outcome. It is what happens when deal enthusiasm overtakes investigative discipline. The best time to discover a problem is before you own it.

The 10 Types of Due Diligence — What Each One Actually Examines

There is no single type of due diligence. A properly structured investigation runs multiple workstreams simultaneously, with specialists leading each area. Here is what each type covers — and why it matters.

1. Financial Due Diligence — The Foundation

Financial due diligence (FDD) validates historical performance and future projections, and produces the Quality of Earnings (QoE) report — the single most important document in any M&A process. The QoE normalizes EBITDA by stripping out one-time items, owner perquisites, accounting distortions, and management discretion to reveal sustainable, recurring profitability.

In India, FDD must verify compliance with Indian Accounting Standards (Ind AS), GST return reconciliation, MCA/ROC-filed financials, and income tax assessment history under the Income Tax Act 2025 (effective April 1, 2026, replacing the 1961 Act with new section references for slump sales, amalgamation loss carry-forward, and transfer pricing).

- Revenue quality — recurring versus one-time, customer concentration, retention rates, deferred revenue

- Working capital normalization — understanding cash required to operate post-acquisition

- Debt structure — term loans, working capital facilities, off-balance-sheet obligations, contingent liabilities

- GST compliance — input credit claims, annual return reconciliation, pending demands

- Deferred tax liabilities and advance tax positions

Cost in India: ₹15–50 lakh for mid-market transactions (deal value ₹50–500 crore). Globally, financial diligence runs 0.5–2% of deal value — accelerated timelines add a 20–40% premium.

2. Legal Due Diligence — Where Deals Quietly Blow Up

Legal diligence covers everything that could create liability, restrict deal completion, or generate post-closing problems. In India, this workstream must navigate the Companies Act 2013 (Sections 129, 133, 134, 177, 178, 230–232), FEMA 1999, SEBI LODR Regulations 17–27 and 23, SEBI Insider Trading Regulations (Regulation 5), and the Insolvency and Bankruptcy Code 2016.

The most dangerous legal risk is the change-of-control clause — a provision in supplier, customer, or landlord contracts that gives the counterparty the right to terminate if ownership changes. These do not appear in financial statements. They are invisible until a lawyer reads the actual contract. They have ended relationships that represented significant revenue — overnight, post-closing.

- ROC filings, DIN verification, board resolutions for major decisions, shareholder agreements

- SEBI compliance — LODR obligations, Regulation 24A secretarial audit reports, insider trading code

- FEMA compliance — FDI/ODI approvals, RBI filings, pricing guideline adherence

- All material contracts reviewed for change-of-control, assignment restrictions, and termination rights

- Litigation — pending, threatened, historical, including NCLT/NCLAT and regulatory proceedings

- Labour law compliance — Industrial Disputes Act, PF, ESIC, gratuity, state-specific legislation

3. Operational Due Diligence — What Are You Actually Inheriting?

Operational diligence goes inside the business. It examines processes, systems, supply chain health, infrastructure condition, and management depth. The critical question: if you acquire this business today, what is the operational reality you are stepping into?

Manufacturing businesses in India often carry risks that do not appear in financial statements — outdated plant and machinery booked at historical cost, heavy vendor concentration in one state, informal contractual arrangements with workers, and ERP systems that cannot integrate with the buyer’s existing infrastructure. These are discovered only through site visits and technical assessment.

- Supply chain — vendor concentration, long-term supply agreements, single-source dependencies

- Plant condition and capacity utilization — verified by chartered engineers via physical inspection

- ERP and IT systems — integration readiness, licensing status, technical debt

- Management depth — key person dependency, succession planning, organizational structure

4. Commercial Due Diligence — Does the Business Model Hold?

Commercial diligence looks outward. It validates the investment thesis by examining the market, competitive position, customer dynamics, and revenue sustainability. Can this business grow — or is the growth story a narrative built on a shrinking base?

| Commercial Diligence Focus | What to Investigate |

|---|---|

| Market size and growth trajectory | Is the TAM expanding or contracting? What drives it? |

| Competitive positioning | Does the company have defensible differentiation? |

| Customer concentration risk | What % of revenue comes from the top 3 customers? |

| Revenue stickiness | Contract lengths, renewal rates, churn data |

| Regulatory environment | How exposed is growth to policy or sector-regulator shifts in India? |

5. Tax Due Diligence — The Silent Deal Killer

Tax diligence is chronically underestimated in Indian mid-market transactions. Companies regularly carry GST demands under objection, income tax assessments at the CIT(A) or ITAT stage, transfer pricing exposures, minimum alternate tax (MAT) credits, and deferred tax liabilities — none of which are obvious from audited financial statements alone.

Cross-border deals add another layer. With the Income Tax Act 2025 effective April 2026, section references for slump sales and amalgamation loss carry-forwards have changed. Buyers must verify the new section mapping before relying on pre-2026 tax opinions.

6. Environmental Due Diligence — Hidden Costs That Can Sink a Deal

In manufacturing, real estate, mining, chemicals, and infrastructure, environmental liabilities can be enormous and entirely invisible until a proper investigation. In India, this means reviewing Environment Protection Act 1986 approvals, pollution control board consents (air and water), hazardous waste authorizations, and EIA clearances for the specific site and use.

A contaminated site can mean crores in remediation, operational shutdowns, and years of regulatory proceedings. At Sapient Services, our chartered engineers have assessed industrial facilities where ground contamination was discovered during technical due diligence — liabilities that were not disclosed, not provisioned, and not visible in any financial record. The deal structure was renegotiated accordingly.

7. IT & Cybersecurity Due Diligence — The New Critical Workstream

79% of deal executives now include cybersecurity diligence in every M&A transaction — up from 52% three years ago. In India, the DPDP Act 2023 adds a specific compliance dimension: any target that processes personal data of Indian users now carries regulatory risk that did not exist in the prior deal cycle.

IT diligence reviews system architecture, software licensing validity, data security posture, technical debt, integration readiness, and active vulnerability exposure. Over 60% of buyers globally have walked away from deals due to cybersecurity concerns — and that number is rising as CERT-In and MeitY enforcement activity increases.

8. HR & Cultural Due Diligence — Soft, But Not Expendable

Research consistently finds that 50–70% of M&A failures are caused by cultural incompatibility — not financial miscalculation. HR diligence reviews employment contracts, compensation benchmarking, ESOP plans and related SEBI compliance, statutory contributions (PF, ESIC, gratuity), talent retention risk, and the distinction between formal and informal workforce arrangements — a significant gap in many Indian mid-market companies.

If the founders won’t stay, the technology the buyer paid for walks out. If the operational teams cannot reconcile different management styles, integration stalls. Cultural diligence is the only workstream that evaluates whether the deal will actually function after it closes.

9. Intellectual Property Due Diligence — Protecting What You Are Paying For

For technology companies, SaaS platforms, pharmaceutical businesses, and brand-driven enterprises, intellectual property may represent the majority of deal value. IP diligence in India verifies registrations under the Trade Marks Act 1999, Patents Act 1970, and Copyright Act 1957 — and, critically, confirms that all IP was formally assigned from founders, employees, and third-party contractors to the company entity.

This is one of the most common serious gaps Sapient’s diligence teams find in Indian startups and technology businesses: IP that the founder developed personally, that was never formally assigned to the company, and that technically does not belong to the entity being acquired.

10. ESG Due Diligence — The 2026 Standard for Institutional Transactions

ESG diligence is no longer optional for institutional buyers. SEBI’s BRSR (Business Responsibility and Sustainability Reporting) framework — mandatory for the top 1,000 listed companies — has established a disclosure baseline that institutional investors are increasingly expecting in private transactions as well.

ESG diligence covers carbon footprint, supply chain labour standards, governance quality, CSR compliance under Section 135 of the Companies Act 2013, board diversity, and alignment with international sustainability frameworks. For transactions involving EU or UK institutional buyers, the EU’s Corporate Sustainability Due Diligence Directive (CSDDD) adds full supply chain accountability requirements.

|

Running a deal and need multi-workstream diligence support? |

The Due Diligence Process in India — Phase by Phase

Due diligence is not a single event. It is a phased, parallel investigation that in India must account for multiple regulatory timelines running simultaneously. A share purchase with no CCI trigger can close in 60–90 days. A scheme of arrangement under Sections 230–232 of the Companies Act runs 6–12 months through the NCLT. Cross-border mergers under Section 234 typically take 9–15 months.

| Phase | Timeline | What Happens |

|---|---|---|

| 1. Preparation | Before LOI | Advisory team assembled, document request list drafted, VDR structure defined, key risk areas identified from preliminary information |

| 2. Information Gathering | Weeks 1–3 | VDR populated, ROC/MCA records verified, all workstreams begin parallel review, access log maintained |

| 3. Deep Analysis | Weeks 3–6 | Financial modeling, contract review clause-by-clause, site visits, management interviews, anomaly investigation |

| 4. Findings & Reporting | Weeks 6–9 | Workstream reports consolidated, red flags documented with quantification where possible, negotiation positions established |

| 5. Decision & Close | Weeks 9–12+ | SPA negotiated based on findings, escrow/indemnity/earnout structures agreed, CCI/SEBI/NCLT/RBI approvals obtained |

Phase 1 — Preparation: Smart buyers begin before the formal process starts. They define the deal thesis, identify known risk areas, and assemble the right team — M&A attorney, transaction CA, IBBI-registered valuer, and where required, a SEBI-registered merchant banker.

Phase 2 — Information Gathering: The buyer’s legal team submits a formal document request list. In India, this includes ROC filings, MCA master data, statutory registers under the Companies Act, FEMA filings for foreign-invested entities, and sector-specific approvals (IRDAI, TRAI, FSSAI, RBI). The VDR is populated — and how organized that VDR is tells you a great deal about the management team you are acquiring.

Phase 3 — Deep Analysis: The most intensive stretch. Financial models are stress-tested. Every material contract is reviewed for non-standard terms and change-of-control provisions. Site visits happen — especially critical for manufacturing, real estate, and infrastructure assets where physical condition must be verified independently of the financial statements.

Phase 4 — Findings & Reporting: All workstreams consolidate into a comprehensive due diligence report. Findings do not automatically kill deals — but they must shape negotiations. Price reductions, escrow holdbacks, earnout structures tied to post-closing performance, and enhanced indemnification provisions all flow directly from this stage.

Phase 5 — Decision & Close: The buyer decides to proceed, renegotiate, or withdraw. If proceeding, required regulatory approvals are obtained: CCI filing (if turnover thresholds are met under the Competition Act as revised in September 2024), SEBI open offer trigger assessment, NCLT approval for scheme-based transactions, and RBI/FEMA compliance for cross-border elements.

Due Diligence in India — What Makes It Different from Global Practice

India’s regulatory architecture is genuinely unique. Buyers who apply a standard international diligence framework without adapting it to India’s multi-regulator environment consistently encounter problems that could have been anticipated. Here is what distinguishes Indian due diligence:

| India-Specific Area | What Due Diligence Must Cover |

|---|---|

| Companies Act 2013 | Sections 129, 133 (financial statements), 134 (board responsibility), 177–178 (audit/nomination committees), 230–232 (merger schemes — NCLT approval required) |

| FEMA 1999 & RBI | FDI/ODI approvals, pricing guideline compliance (FEMA (Non-Debt Instruments) Rules 2019), annual return on foreign liabilities, RBI filings |

| SEBI (listed entities) | LODR Regulations 17–27 (governance), Regulation 23 (related-party), Regulation 24A (secretarial audit), Takeover Code open offer trigger at 25% |

| IBC 2016 | History of insolvency proceedings, NCLT/NCLAT orders, any moratorium provisions, resolution plan covenants that survive the plan period |

| Income Tax Act 2025 | New section references effective April 2026 for slump sales, amalgamation loss carry-forward, transfer pricing — pre-2026 opinions must be reverified |

| GST | GST returns reconciliation with financials, input credit claims, pending demands and assessments, annual return filing status |

| DPDP Act 2023 | Data processing inventory, consent management framework, data localisation obligations — creates compliance risk for any target handling Indian user data |

| CCI (Competition Act, revised Sept 2024) | New deal value thresholds under the revised merger control regime — now includes transaction value in addition to turnover/asset tests |

|

From Sapient Services’ experience in Indian mid-market transactions: The four most consistently discovered red flags are: (1) undisclosed GST demands or assessment orders under appeal, (2) ROC filing gaps and non-compliance with Section 134 annual report obligations, (3) informal employment arrangements — key operators on the payroll of a related entity, not the company being acquired, and (4) IP developed by the founder personally that was never formally assigned to the company. None of these appear in audited financial statements. All four materially affect deal value. |

From the Field — How Due Diligence Actually Works in Practice

Sapient Services Case Context: Manufacturing Acquisition, North India

|

Situation: What We Found: Outcome: |

The HP-Autonomy Case: What USD 8.8 Billion of Skipped Diligence Looks Like

HP paid USD 11.1 billion to acquire Autonomy, a UK software company, in 2011. Within a year, it wrote down USD 8.8 billion — attributing USD 5 billion to accounting irregularities. Autonomy had been treating hardware sales as software revenue and using round-trip transactions to inflate earnings. The investigation that preceded this commitment reportedly involved four conference calls totaling roughly six hours.

In July 2025, the UK High Court ruled that Lynch’s estate and former CFO owe HPE approximately £740 million (~USD 940 million) in damages — far below the USD 4–5 billion HPE had originally claimed. The judge himself noted that HP’s damages claim was “substantially exaggerated.” The lesson is not about the final damages number. It is about what the investigation missed: years of revenue misclassification that went undetected, and a write-down of USD 8.8 billion within twelve months of closing. Deal momentum cannot override investigative discipline.

Common Due Diligence Mistakes — And How to Avoid Them

Most problems in post-closing integration were visible during diligence — they were either missed or not acted on. Here are the most consistent mistakes:

- Artificial time pressure is the single biggest driver of diligence failure. If you cannot negotiate adequate time, price the compressed risk explicitly into your deal terms or offer price. Rushing to beat a competing bidder

- HP had a KPMG diligence report on Autonomy. The CFO received it and never read it. The report means nothing if the findings do not shape negotiations. Not acting on findings

- These are in supplier contracts, customer agreements, landlord leases, and distribution arrangements. A contract review that is not specifically looking for them will miss them. Missing change-of-control clauses

- With 50–70% of M&A failures driven by cultural incompatibility, this is statistically the highest-probability risk in most deals. Skipping it entirely is not minor negligence. Treating cultural fit as a formality

- Especially in Indian technology and SaaS deals — if the founder built the core technology before incorporation or as an individual, that IP may not legally belong to the company being acquired. Ignoring IP assignment gaps

- India has state-specific industrial legislation. A diligence that only checks the Contract Labour Act and IDA without reviewing state-level Shops & Establishments Act compliance and applicable state rules will miss material non-compliance. Relying solely on central labour laws

- A statutory audit confirms financial statement accuracy. It does not verify GST return reconciliation, pending demand orders, or ITC reversal obligations — these require a separate tax workstream. Not verifying GST separately from the financial audit

Pro Tips: What Experienced Acquirers Do Differently

These are not theoretical suggestions. They are patterns we observe consistently in well-run Indian M&A transactions:

|

Tip 1: Start with the customer list — not the financial statements. Tip 2: Send a chartered engineer for asset-heavy businesses — not just an accountant. Tip 3: Engage the seller’s key employees — not just the founders. Tip 4: Reverse-engineer the projected growth to stress-test the valuation. Tip 5: Build a post-closing integration plan during diligence — not after. |

Complete Due Diligence Checklist for India M&A Transactions (2026)

This checklist is structured for Indian transactions. Adapt scope based on deal size, industry, and whether the target is listed, foreign-invested, or IBC-distressed.

| Workstream | Key Items to Verify |

|---|---|

| Corporate Structure | Certificate of Incorporation, MoA/AoA, ROC/MCA filings (3–5 years), DIN verification, cap table, subsidiary structures, any holding company obligations |

| Financial Records | 3–5 years audited financials (Ind AS), monthly management accounts (24 months), QoE report, working capital analysis, debt schedule, off-balance-sheet obligations |

| Tax Compliance | Income Tax returns (6 years), pending assessments and appeals, GST returns reconciliation, TDS filings, transfer pricing documentation, advance tax position, MAT credits |

| Legal & Contracts | All material contracts with change-of-control review, NDA agreements, pending/threatened litigation, ROC compliance with Section 134, regulatory approvals and licences |

| SEBI / Capital Markets | LODR compliance history, Regulation 24A secretarial audit reports, insider trading code, shareholding pattern, open offer trigger assessment under Takeover Code |

| IBC & Insolvency History | NCLT/NCLAT proceedings history, IBBI filings, any moratorium or resolution plan covenants surviving the plan, DRT/SARFAESI matters |

| Intellectual Property | TM, patent, copyright registrations; assignment agreements from founders, employees, third-party contractors; open-source licence audit; freedom-to-operate assessment |

| HR & Labour | Employment contracts (key employees), PF/ESIC/gratuity compliance, ESOP documentation and SEBI compliance, state-specific labour law adherence, contractor/casual workforce arrangements |

| Operations & Assets | Chartered engineer inspection of key assets, plant capacity utilization, supply chain concentration, IT systems and ERP assessment, key operational approvals and licences |

| Environmental | PCB consents (air and water), EIA clearances, hazardous waste authorizations, Environment Protection Act approvals, site contamination assessment (manufacturing and industrial) |

| IT & Cybersecurity | DPDP Act 2023 compliance review, data processing inventory, security posture assessment, software licence audit, CERT-In incident reporting compliance |

| ESG / Governance | BRSR disclosures for listed entities, CSR compliance (Section 135 Companies Act), board composition, governance audit, supply chain labour standards |

How AI Is Changing Due Diligence in 2026

AI tools now reduce document review time by 50–70% and improve anomaly detection accuracy by 20–30%, according to Deloitte research. Nearly 57% of diligence professionals globally now use AI-driven analytics in their review process — and adoption in Indian advisory firms is accelerating alongside deal volume growth.

| AI Application | Practical Impact |

|---|---|

| Contract review and clause extraction | Scans thousands of agreements in hours, flags non-standard terms, change-of-control provisions, and unusual termination clauses |

| Financial anomaly detection | Identifies duplicate invoicing, unusual related-party transactions, and revenue recognition inconsistencies that exhausted human reviewers miss |

| Regulatory compliance screening | Cross-references against MCA/ROC records, sanctions lists, PEP databases, and SEBI enforcement actions simultaneously |

| VDR organisation and indexing | Auto-categorises uploaded documents, reduces setup time, improves workstream coordination — cutting adviser time by 25–35% |

| Predictive scenario modeling | Forecasts revenue, cash flow, and market risk across deal structures and economic scenarios |

That said, AI does not replace judgment. A tool can flag a clause as non-standard. Only an experienced M&A lawyer can tell you whether it will actually affect the transaction — and how to negotiate around it. The firms delivering the best outcomes are those combining AI-powered efficiency with domain-specific human expertise.

|

Have a deal situation similar to what you read above? |

Frequently Asked Questions

What does due diligence mean in simple terms?

Due diligence means doing your homework before a major financial commitment. It is the process of independently verifying all material facts about a business or asset before you sign a contract or transfer money. In legal terms, it refers to the reasonable care a person must take before entering a transaction. In business, it has grown into a structured investigation covering financial records, legal compliance, operational health, and regulatory standing.

Who conducts due diligence in India?

A typical Indian M&A due diligence team includes a Chartered Accountant firm (financial and tax workstreams), an M&A law firm (legal workstream), IBBI-registered valuers (for share swap ratios under Section 247 of the Companies Act and IBC-related assignments), chartered engineers (for technical and operational assessment of asset-heavy businesses), and HR consultants (for cultural and workforce analysis). For cross-border deals, FEMA specialists and merchant bankers are added.

What are the most important types of due diligence in India?

For Indian M&A transactions, the most critical workstreams are financial due diligence (QoE report, GST compliance, tax positions), legal due diligence (contract review with change-of-control analysis, SEBI/FEMA/Companies Act compliance), and operational due diligence (physical asset verification, supply chain assessment). For technology deals, IP and cybersecurity diligence are equally critical. For any listed company acquisition, SEBI LODR compliance and open offer trigger assessment are non-negotiable.

How long does due diligence take in India?

Timeline varies significantly by deal structure. A straightforward unlisted share purchase with no CCI filing requirement typically completes in 45–90 days. A scheme of arrangement under Sections 230–232 of the Companies Act 2013, requiring NCLT approval, runs 6–12 months. Cross-border mergers under Section 234 take 9–15 months. Banking and insurance acquisitions requiring RBI or IRDAI approval routinely exceed 12–18 months. Distressed acquisitions through IBC resolution processes depend on NCLT timelines.

How much does due diligence cost in India?

Due diligence costs in India range from ₹10–30 lakh for straightforward legal and financial review of smaller businesses, to ₹1–5 crore or more for complex M&A transactions involving multiple workstreams. As a proportion of deal value, total diligence costs typically run 0.5–2%. Compressed timelines add a 20–40% premium. An organized Virtual Data Room on the seller’s side can reduce buyer-side adviser time by 25–35%, materially reducing cost.

What is a Quality of Earnings (QoE) report?

A Quality of Earnings report is the primary deliverable of financial due diligence. It normalizes a company’s reported EBITDA by removing one-time items, adjusting for accounting inconsistencies, and presenting a true picture of sustainable, recurring profitability. In Indian transactions, this commonly involves reversing capitalized maintenance costs, adjusting for related-party transactions at non-arm’s-length pricing, and normalizing owner compensation. The QoE is the document most frequently responsible for deal price renegotiation.

What is Enhanced Due Diligence (EDD)?

Enhanced Due Diligence is a deeper level of investigation required for higher-risk counterparties — including high-value transactions, Politically Exposed Persons (PEPs), entities with complex ownership structures, and businesses operating in high-risk sectors or jurisdictions. In India, EDD is required under the Prevention of Money Laundering Act 2002 (PMLA) for financial institutions, and is increasingly standard in cross-border private equity transactions. It involves deeper background verification, source-of-funds analysis, and beneficial ownership investigation beyond standard KYC.

What is a Virtual Data Room (VDR)?

A VDR is a secure online repository where the seller organizes and shares documents for buyer review during the due diligence period. It replaces physical data rooms, allows multiple workstream teams to work simultaneously, controls access by document category, and maintains a complete audit trail of reviewer activity. For Indian transactions — which involve ROC filings, MCA records, statutory registers, SEBI disclosures, and sector regulator approvals — how a seller organizes the VDR signals a great deal about management quality before investigation even begins.

What are the most common red flags found in Indian due diligence?

Based on Sapient Services’ transaction experience: undisclosed GST demands or income tax assessments under appeal; revenue that is suspiciously smooth relative to industry volatility; customer concentration above 30–40% in one account with no long-term contract; IP that was created by the founder personally and never formally assigned to the company; ROC filing gaps and secretarial non-compliance; informal workforce arrangements where key operators are on the payroll of a related entity rather than the target company; and FEMA non-compliance in entities with foreign investment history.

Can due diligence findings kill a deal?

Yes — and sometimes they should. More often, findings reshape deals rather than terminate them. Typical outcomes include price reductions (the most common result), escrow holdbacks for identified contingent liabilities, representations and warranties insurance to transfer specific risks to an insurer, enhanced indemnification caps, and earnout structures that tie consideration to post-closing performance. The measure of good diligence is not whether it kills deals — it is whether it ensures that buyers know exactly what they are getting and price it accordingly.

Does Sapient Services provide due diligence services?

Yes. Sapient Services Pvt. Ltd. provides financial, operational, and technical due diligence services for M&A transactions, bank lending, private equity investments, and corporate restructuring. Our team includes IBBI-registered valuers under the Companies Act 2013, chartered engineers, and transaction specialists with over four decades of experience across sectors including power, manufacturing, infrastructure, financial services, pharmaceuticals, and real estate. We operate from New Delhi and have worked on assignments across India and in 16+ countries.

Have more questions? Contact our team directly at valuation@sapientservices.com or +91 9540162888.

Conclusion — Due Diligence Is Not an Expense. It Is the Investment.

The cost of due diligence — in time, fees, and management attention — is not overhead on a deal. It is the single most cost-effective investment a buyer can make. A ₹25 lakh investigation that uncovers a ₹50 crore liability or prevents a value-destroying acquisition is not an expense. It is a return.

India’s deal market is growing faster than the advisory infrastructure that serves it. As M&A activity reaches USD 123.8 billion annually and regulatory complexity compounds — with the Income Tax Act 2025, DPDP Act 2023, revised CCI thresholds, and SEBI’s evolving Takeover Code — the gap between buyers who investigate thoroughly and those who do not is widening.

If you are approaching a transaction — whether as a buyer, an investor, a bank, or a Resolution Professional under IBC 2016 — the question is not whether you can afford proper due diligence. The question is whether you can afford to skip it.

| Need due diligence support for your next transaction?

Sapient Services Pvt. Ltd. | IBBI Registered Valuers | New Delhi +91 9540162888 | valuation@sapientservices.com | sapientservices.com Sapient House, S-15, Pocket S, Okhla Phase II, New Delhi — 110020 |