New Income Tax Act vs Old Act: Key Valuation and M&A Provisions That Changed in 2026

By

By

India’s tax code changed permanently on 1 April 2026. The Income Tax Act, 2025 replaced the Income Tax Act, 1961 — a law that had accumulated over 4,000 amendments across six decades. For M&A advisers, IBBI-registered valuers, and CFOs handling business restructuring, this is not a simple renumbering exercise.

Several provisions governing slump sale valuations, fair market value (FMV) computation, merger loss carry-forwards, and capital gains on business transfers have been substantively revised. A post-April 2026 transaction computed under old rules will produce incorrect capital gains figures and may invite scrutiny.

This article covers the five most consequential changes — what the old Act said, what the new Act says, and what your team needs to update before the next deal closes.

| Need a valuation report compliant with the new Income Tax Act, 2025? Contact Sapient Services — IBBI Registered Valuers, New Delhi. Visit sapientservices.com |

Quick Overview:

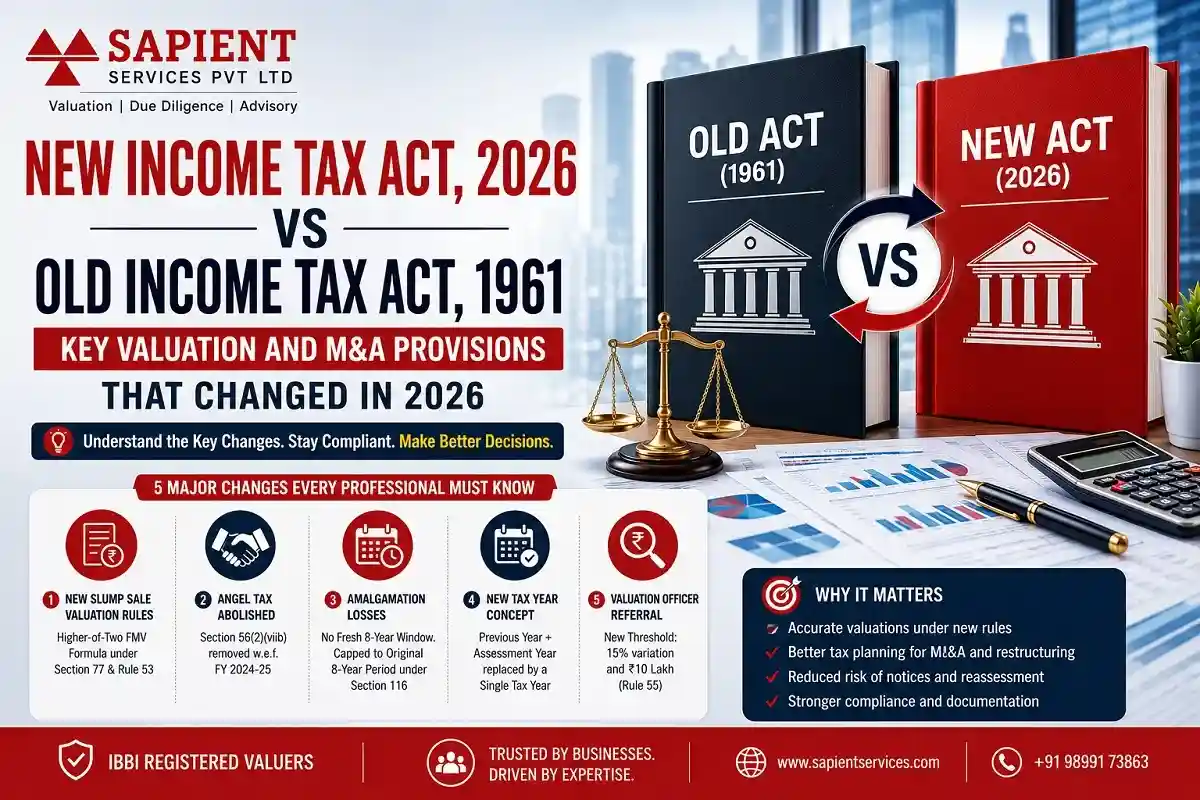

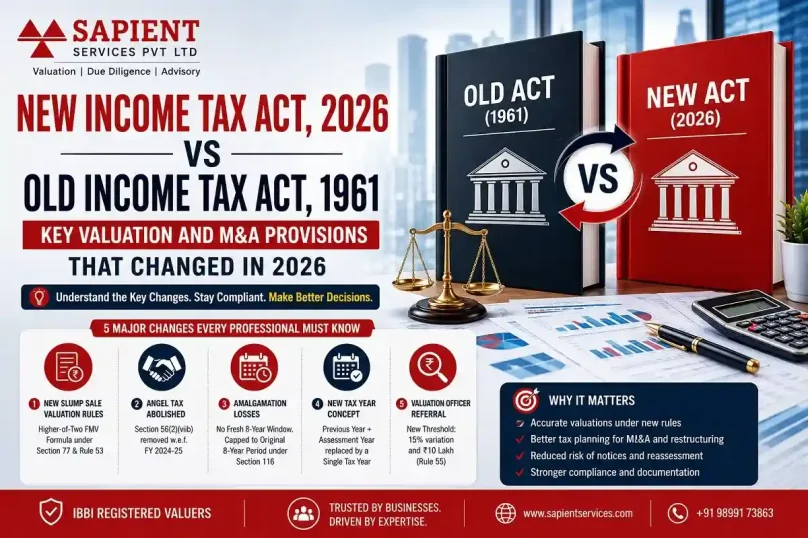

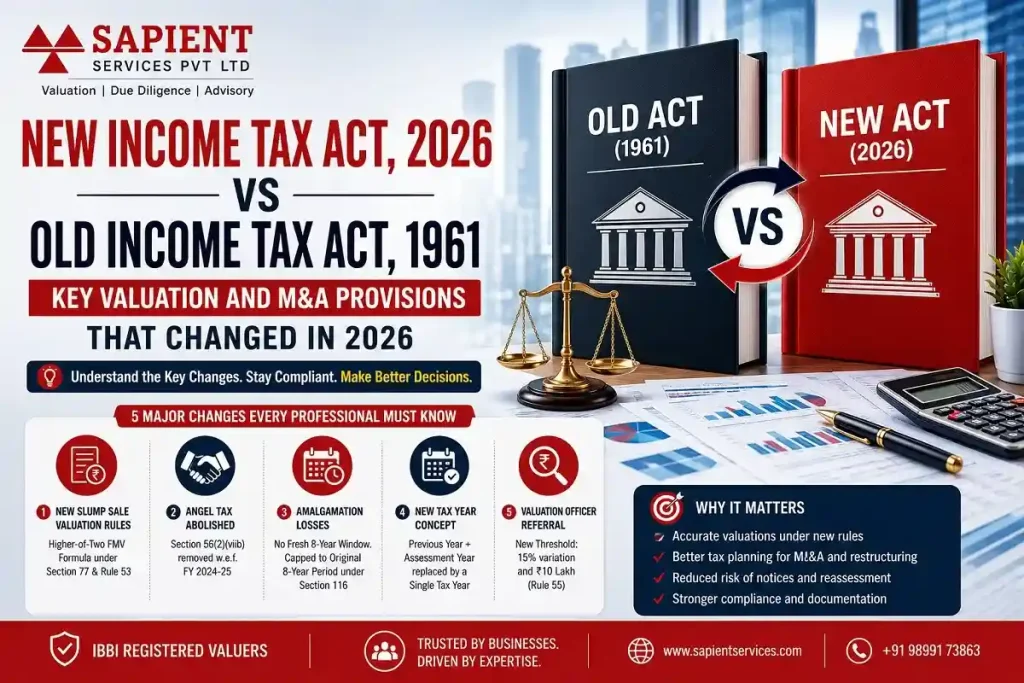

- Income Tax Act, 2025 (effective from 1 April 2026) reduces the law from 819 sections to 536 sections.

- Key changes impacting M&A and valuation:

- Slump Sale FMV: Now governed by Section 77, with a mandatory higher-of-two valuation formula under Rule 53 of the Income Tax Rules, 2026.

- Angel Tax Removed: Old Section 56(2)(viib) has been abolished from FY 2024–25, with no replacement provision in the new Act.

- Amalgamation Losses: Under Section 116, merger losses cannot be reset for a fresh 8-year carry-forward period; the original computation date continues.

- Single Tax Year Concept: Assessment Year (AY) and Previous Year (PY) are replaced with one unified “Tax Year.”

- Valuation Officer Referral Threshold: Under Rule 55, referral applies only if the valuation difference exceeds both 15% and ₹10 lakh.

What Is the New Income Tax Act, 2025?

The Income Tax Act, 2025 is India’s new direct tax law, effective from 1 April 2026, replacing the Income Tax Act, 1961. It applies to all income earned from Tax Year 2026-27 onwards. The old Act continues to govern FY 2025-26 income, and all pending assessments and proceedings under it continue until final resolution.

The restructuring reduces 819 sections to 536 across 23 chapters — not by removing tax benefits, but by eliminating redundant provisos, embedding explanations into main text, and replacing narrative clauses with tables and formulas. Tax rates, deductions, and the fundamental scheme of taxation are unchanged.

What changed for M&A and valuation professionals is the section references, the FMV computation methodology for slump sales, and the rules governing accumulated losses in mergers. These are not cosmetic changes — they affect how capital gains are calculated and how much tax shields an acquirer can actually use.

| Parameter | Income Tax Act, 1961 | Income Tax Act, 2025 |

| Effective from | April 1, 1962 | April 1, 2026 |

| Total sections | 819 sections | 536 sections |

| Applies to | AY 2026-27 and earlier | Tax Year 2026-27 onwards |

| Time concept | Previous Year + Assessment Year | Single Tax Year |

| Rules framework | Income Tax Rules, 1962 (511 rules, 399 forms) | Income Tax Rules, 2026 (333 rules, 190 forms) |

| Slump sale provision | Section 50B + Rule 11UAE | Section 77 + Rule 53 (higher-of-two FMV) |

| FMV certification form | Form 3CEA | Form No. 28 under Rule 54 |

| Amalgamation losses | Sec 72A — fresh 8-year window post-merger | Sec 116 — capped to original 8-year window |

| Angel tax | Section 56(2)(viib) — abolished from Apr 2025 | No equivalent provision |

Who Needs to Understand These Changes — and Why It Matters

These provisions affect every professional involved in Indian corporate restructuring and business transfers:

- IBBI Registered Valuers preparing FMV reports for slump sales and demergers must now follow Rule 53 of the Income Tax Rules, 2026 — the two-tier FMV formula replaces the single-method Rule 11UAE approach.

- M&A advisers and investment bankers modelling post-merger synergies must recalculate loss carry-forward timelines. A target company’s Rs. 50 crore loss shield does not automatically give the acquirer a new 8-year runway under Section 116.

- Chartered Accountants certifying net worth for slump sale purposes must use Form No. 28 under Rule 54 and file it with the ITR. The old Form 3CEA no longer applies.

- CFOs and corporate tax teams must update all internal valuation templates, deal memos, and correspondence to reference new section numbers.

- Resolution Professionals under IBC must confirm whether a transaction’s effective date falls before or after 1 April 2026, which determines which Act applies.

Miss these changes, and the consequences are direct: an incorrectly computed slump sale capital gain filed under old rules will show up as a discrepancy when cross-checked against the Valuation Officer’s computation under Rule 53. Reassessment risk is real.

Change 1 — Slump Sale Capital Gains: New FMV Formula Under Section 77

Old Act: Section 50B and Rule 11UAE

Under the Income Tax Act, 1961, slump sale capital gains were governed by Section 50B. The full value of consideration for capital gains purposes was the FMV of the transferred undertaking, computed under Rule 11UAE of the Income Tax Rules, 1962. The net worth of the undertaking — aggregate assets less specified liabilities, excluding revaluation reserves — was the cost of acquisition.

New Act: Section 77 and Rule 53 — Higher-of-Two Formula

Under Section 77 of the Income Tax Act, 2025, the FMV of capital assets transferred in a slump sale is determined using Rule 53 of the Income Tax Rules, 2026. The rule prescribes a two-tier approach: capital gains are computed on the higher of FMV1 or FMV2.

- FMV1 (Asset-based): Aggregate book value of all assets transferred, adjusted to include the registered valuer’s market value for jewellery and artistic works, Rule 57 FMV for shares and securities, and stamp duty value of immovable property — reduced by book value of specified liabilities (excluding equity capital, reserves, unascertained provisions, and contingent liabilities).

- FMV2 (Consideration-based): Total monetary consideration plus FMV of non-monetary consideration, including stamp duty value of immovable property and valuation-based pricing for other assets.

Valuation is determined as on the date of slump sale. The higher-of-two formula is explicitly anti-avoidance — it closes the earlier loophole where consideration could be structured below asset-book values to suppress capital gains.

| Provision | Old Act (1961) → New Act (2025) |

| Governing section | Section 50B → Section 77 |

| FMV computation rule | Rule 11UAE → Rule 53 (Income Tax Rules, 2026) |

| FMV approach | Single method → Higher of FMV1 or FMV2 |

| Accountant certification form | Form 3CEA → Form No. 28 (Rule 54) |

| Filing requirement | With ITR → Mandatory with ITR (no separate filing) |

| Valuation date | Date of slump sale → Date of slump sale (Rule 53(4) confirms) |

| Valuation Officer referral | Discretionary → Triggered at 15% variance + Rs. 10 lakh (Rule 55) |

What This Means in Practice

Any business transfer structured as a slump sale with an effective date on or after 1 April 2026 must be valued under Rule 53. The certifying accountant must compute both FMV1 and FMV2, pick the higher, and certify it in Form No. 28 — not the old Form 3CEA format.

In asset-heavy industries — manufacturing, logistics, real estate — FMV1 (asset-based) typically governs. In IP-rich or brand-led businesses where agreed consideration exceeds book values, FMV2 will be higher. The rule requires the higher figure to be used regardless of what was contractually agreed.

| Need a Rule 53-compliant FMV report for a slump sale? Sapient Services prepares Form No. 28-ready valuations for IBBI Registered Valuers and CAs. Request a consultation — +91 9540162888 |

Change 2 — Angel Tax Abolished: No Equivalent in the New Act

Under the Income Tax Act, 1961, Section 56(2)(viib) taxed unlisted companies that issued shares at a premium above fair market value. The excess consideration was taxable as ‘Income from other sources.’ This provision — commonly called angel tax — was a persistent source of litigation and valuation disputes for startups and closely held companies.

The Finance Act, 2024 abolished angel tax with effect from 1 April 2025. The Income Tax Act, 2025 carries no equivalent provision. What this means for valuation work:

- Unlisted companies raising equity at a premium above FMV will not face any income tax demand on the difference under the new Act.

- Valuers and SEBI Category I Merchant Bankers preparing share valuation reports for funding rounds now face zero angel tax dispute risk. Their reports serve SEBI, Companies Act, and ESOP compliance — not income tax defence.

- FMV requirements for ESOPs under Section 17(2), offshore share transfers under Section 9, and transfer pricing under Section 161 of the new Act continue unchanged.

For a Delhi-based startup raising a Series A in 2026: the share valuation exercise is now about regulatory compliance, not income tax protection. The risk that drove many founders to over-engineer their valuation reports is gone.

Change 3 — Amalgamation Loss Carry-Forward: Section 116 Caps the Window

The Old Rule and the Loophole

Under old Sections 72A and 72AA of the Income Tax Act, 1961, when a company was acquired through merger, the successor entity could carry forward the predecessor’s accumulated losses for a fresh 8-year period from the year of amalgamation. Each merger effectively reset the loss carry-forward clock, allowing companies to roll over tax losses indefinitely through successive restructuring.

The Finance Act, 2025 inserted sub-section (6B) into Section 72A to close this. The amendment applies to amalgamations effected on or after 1 April 2025 and is now carried into the Income Tax Act, 2025 under Sections 116 and 117.

What Section 116 of the New Act Says

Accumulated losses of a predecessor entity can be carried forward by the successor only for the balance of the original 8-year period — counted from the year the loss was first computed by the original entity, not from the year of amalgamation. The carry-forward period does not reset after a merger.

Section 536(2)(m) of the new Act expressly provides that losses brought forward from before 1 April 2026 continue to be eligible for carry-forward under the new Act, but the total period cannot exceed the original 8-year window.

| Scenario | Impact Under New Act |

| Predecessor’s losses have 6 years remaining at merger date | Successor gets only 6 years — not a fresh 8 years |

| Serial amalgamations to extend loss shield | No longer possible — 8-year clock anchored to original computation year |

| Losses first computed before 1 April 2026 | Carry-forward continues but subject to original 8-year limit (Section 536 transitional) |

| Unabsorbed depreciation | No time cap — carries forward without restriction (unchanged) |

| Banking sector amalgamations | Governed by Section 117 — special provisions apply |

| Strategic disinvestment cases | Specific provisions under Section 116 sub-clauses — consult adviser |

Impact on M&A Valuation Models

In distressed asset acquisitions and IBC resolution scenarios, accumulated tax losses have historically been valued as part of deal consideration. A company with Rs. 40 crore of brought-forward losses that has 3 years remaining does not give the acquirer a new 8-year shield — only 3 years remain usable.

This changes the tax synergy component of any DCF model for such acquisitions. M&A teams that have not updated their models to reflect the Section 116 restriction are overstating the tax benefit and, consequently, the fair market value of the acquisition target.

Change 4 — Tax Year Replaces Assessment Year and Previous Year

The Income Tax Act, 2025 eliminates the dual concept of Previous Year and Assessment Year and replaces both with a single Tax Year. Tax Year 2026-27 runs from 1 April 2026 to 31 March 2027 — income earned in that period is assessed and filed under the same Tax Year label.

For valuation professionals, the practical impact is on documentation: all reports, certificates, computation sheets, and accountant certifications for post-April 2026 transactions must reference the Tax Year, not the Assessment Year. The income tax portal Tab 2 uses new Act references from Tax Year 2026-27 onwards; Tab 1 continues for FY 2025-26 returns filed in July 2026.

Pending assessments, appeals, and proceedings under the 1961 Act continue under the old Act’s provisions — the transition is entirely prospective. Options exercised under the old Act (such as new tax regime elections) are treated as if made under the equivalent provision of the new Act.

Change 5 — Valuation Officer Reference: Dual Threshold Under Rule 55

Under Rule 55 of the Income Tax Rules, 2026, an Assessing Officer can refer a case to a Valuation Officer under Section 91(1)(b)(i) of the new Act when two conditions are simultaneously met: the declared value of an asset varies from the AO’s assessment by 15% or more, and the absolute difference amounts to Rs. 10 lakh or more.

The dual condition — percentage threshold plus absolute floor — is a refinement from the earlier framework and reduces automatic referrals for smaller transactions. For M&A advisers and valuers, this means a well-documented valuation report from an IBBI Registered Valuer is your primary defence against a Valuation Officer reference. If your declared FMV and the AO’s estimate diverge by less than 15%, or the absolute gap is under Rs. 10 lakh, a referral cannot be made.

A Practical Note From Sapient’s Valuation Desk

One assignment our team handled in early 2026 involved a manufacturing group planning to hive off a business division through a slump sale. The transaction had been structured and pre-computed under Rule 11UAE — the old framework. The effective transfer date fell in April 2026, making the new Act applicable.

The recomputation under Rule 53 revealed that FMV2 (consideration-based) exceeded FMV1 (asset-based) by 11%. Under the old approach, capital gains would have been understated. The team also needed to update the accountant certification to Form No. 28 format under Rule 54, replacing the draft that had been prepared in the old Form 3CEA style.

The revised computation went into the ITR without incident. For the acquirer’s team, a separate review of the predecessor’s loss carry-forward schedule revealed that only 4 years of the original 8-year window remained — not 8 fresh years as the initial deal model had assumed. The deal pricing was adjusted accordingly.

Common Errors Post-April 2026 — What to Watch For

Mistake 1: Citing Section 50B or Rule 11UAE for post-April 2026 slump sales. These provisions do not apply to transactions effective on or after 1 April 2026. The correct references are Section 77 of the Income Tax Act, 2025 and Rule 53 of the Income Tax Rules, 2026. Using old references in valuation reports or ITR schedules creates a direct compliance discrepancy.

Mistake 2: Using old FMV templates without computing FMV2. Rule 53 requires both FMV1 and FMV2 to be computed — not just the asset-based calculation. In deals where consideration exceeds book value, FMV2 governs. Skipping this step produces an understated capital gain.

Mistake 3: Assuming a fresh 8-year loss window post-merger. Under Section 116 of the new Act, no fresh carry-forward period is granted after an amalgamation. The 8-year clock runs from the year losses were first computed by the original predecessor. This is the highest-value error in M&A due diligence right now.

Mistake 4: Filing old Form 3CEA instead of new Form No. 28. Rule 54 requires Form No. 28 to be filed along with the ITR for slump sales under Section 77(4). The form must be filed with the return — not after. Old Form 3CEA certifications are not valid for post-April 2026 transactions.

Mistake 5: Mixing Assessment Year and Tax Year terminology. All documents, notices, and filings for Tax Year 2026-27 onwards use Tax Year references. Using Assessment Year terminology post-April 2026 in formal documents creates confusion in assessment proceedings and may require corrections.

Pro Tips for Valuers and M&A Advisers

Tip 1: Update all valuation report templates before the next mandate. Every template that references Section 50B, Section 56(2)(viib), or Rule 11UAE for income tax purposes needs to be revised. The corresponding new references are Section 77 (slump sale), Section 91 (Valuation Officer), and Rule 53/Rule 57 (FMV computation).

Tip 2: Always compute both FMV1 and FMV2 for slump sales. Do not assume FMV1 is always higher. For IP-rich, brand-heavy, or going-concern businesses where agreed consideration exceeds asset book value, FMV2 governs. Document both figures in the report and state the applicable one clearly.

Tip 3: In M&A due diligence, map the year each loss was first computed. For any target company with brought-forward losses, request the year-wise loss computation history going back to the first year of origination. Under Section 116, the carry-forward period counts from that year — not from the acquisition date. Revise DCF models accordingly.

Tip 4: Check effective date, not agreement date, for Act applicability. The Income Tax Act, 2025 applies to transactions with an effective date on or after 1 April 2026. A slump sale agreement signed in January 2026 but effective in April 2026 is governed by the new Act. Confirm effective dates before drafting accountant certifications.

Tip 5: File Form No. 28 with the ITR — it cannot be a subsequent filing. Rule 54 is clear: the accountant’s report in Form No. 28 must be submitted along with the return of income. Ensure your CA team completes the Form No. 28 certification, including both FMV computations and net worth workings, before the ITR is filed.

Tip 6: Build a documentation buffer if FMV is close to the Rule 55 threshold. Where your declared FMV and a probable AO estimate are within 20% of each other and the absolute difference could approach Rs. 10 lakh, prepare a detailed methodology note. A well-supported IBBI Registered Valuer report with documented assumptions substantially reduces Valuation Officer referral risk.

| M&A transactions, slump sales, or demerger valuations after April 2026? We can help with similar cases. Contact Sapient Services — sapientservices.com | +91 9540162888 |

Frequently Asked Questions

Q1. What is the Income Tax Act, 2025 and from when does it apply?

The Income Tax Act, 2025 replaced the Income Tax Act, 1961 from 1 April 2026. It applies to income from Tax Year 2026-27 onwards. FY 2025-26 income continues to be governed by the old Act.

Q2. What section governs slump sale capital gains under the new Act?

Section 77 of the Income Tax Act, 2025 governs slump sale capital gains (previously Section 50B). FMV computation is under Rule 53 of the Income Tax Rules, 2026, using the higher of FMV1 (asset-based) or FMV2 (consideration-based).

Q3. Is angel tax still applicable after 1 April 2026?

No. Angel tax under old Section 56(2)(viib) was abolished from 1 April 2025 via the Finance Act, 2024. The Income Tax Act, 2025 has no equivalent provision — unlisted companies issuing shares above FMV face no income tax liability on the premium.

Q4. Can accumulated losses still be carried forward after a merger under the new Act?

Yes, but only for the balance of the original 8-year period from when the loss was first computed by the predecessor — not for a fresh 8 years from merger date. This restriction under Section 116 applies to amalgamations effected on or after 1 April 2025.

Q5. What is the new form required for slump sale accountant certification?

Form No. 28 under Rule 54 of the Income Tax Rules, 2026 replaces the old Form 3CEA. It must be filed along with the ITR for slump sales under Section 77(4) and requires separate FMV1 and FMV2 computations alongside the net worth workings.

Q6. What replaced the Assessment Year and Previous Year concept?

The Income Tax Act, 2025 replaced both with a single Tax Year. Tax Year 2026-27 covers 1 April 2026 to 31 March 2027 — income earned in that period is assessed and filed under the same label.

Q7. When can an AO refer a case to a Valuation Officer under the new rules?

Under Rule 55 of the Income Tax Rules, 2026, a referral to a Valuation Officer requires two conditions to be simultaneously met: the asset value varies by 15% or more from the declared figure, and the absolute difference is Rs. 10 lakh or more.

Q8. Does the new Act change FMV computation for share transfers?

The basic framework continues under Rule 57 of the Income Tax Rules, 2026 (corresponding to old Rule 11UA). The definition of merchant banker for share valuation purposes remains a SEBI-registered Category I Merchant Banker. DCF and net asset value methods for unquoted shares remain available.

Q9. If a slump sale agreement was signed before April 2026 but closes after, which Act applies?

The applicable Act depends on the effective date of transfer, not the agreement date. A transaction effective on or after 1 April 2026 falls under the new Act — FMV computation, accountant certification, and section references must all align with the Income Tax Act, 2025 and Income Tax Rules, 2026.

Q10. Do pending assessments under the old Act continue after April 2026?

Yes. Section 536 of the Income Tax Act, 2025 contains transitional provisions. All proceedings pending under the 1961 Act continue under the old Act until final resolution. Losses carried forward from before 1 April 2026 also continue under the new Act per Section 536(2)(m), subject to the original carry-forward period.

| Have more questions about valuation compliance under the new Act? Contact our team: +91 9540162888 | valuation@sapientservices.com |

Conclusion

The Income Tax Act, 2025 is not a cosmetic reprint of the 1961 Act. For M&A and valuation professionals, three changes carry direct financial risk: the new two-tier FMV formula for slump sales under Rule 53, the capped amalgamation loss carry-forward under Section 116, and the formal abolition of angel tax with no successor provision.

Transactions executing after 1 April 2026 that are computed under old rules will produce incorrect capital gains figures, use the wrong accountant certification form, and may overstate the tax synergy value of merger targets. Update your templates, recalibrate your deal models, and confirm effective dates before any post-April 2026 transaction is signed off.

If you need a valuation report for a slump sale, M&A deal, ESOP grant, or regulatory purpose under the new Income Tax Act, 2025, contact Sapient Services at +91 9540162888 or visit sapientservices.com.

Suggested Services