What Is an IPO? Meaning, Process & Types Explained

By

By

India has consistently ranked among the world’s busiest IPO markets by number of listings in recent years, with hundreds of companies going public across Mainboard and SME platforms every year. Yet most first-time promoters and new investors still ask the same basic question: what exactly is an IPO, and what actually happens between a company deciding to go public and its shares trading on your screen?

An IPO, or Initial Public Offering, is the process through which a private company sells shares to the public for the first time and becomes a publicly listed company. This guide breaks down what an IPO means, how the process works in India, the types of IPOs, and what both companies and investors need to know before one begins.

|

Quick Overview

|

What Does IPO Mean?

IPO stands for Initial Public Offering. It is the process by which a privately held company offers a portion of its ownership to the public for the first time, in exchange for capital. Once the IPO is complete, the company’s shares trade freely on a stock exchange such as the NSE or BSE.

Before an IPO, a company’s shares are held by a small group — promoters, founders, and private investors. An IPO changes that. It opens the ownership base to institutional investors, high-net-worth individuals, and retail investors, while giving the company access to public capital markets for the first time.

Private Company vs Public Company: What Changes

Going public is a legal and structural shift, not just a fundraising event. A public company must publish audited financials regularly, disclose material events to the stock exchanges, and answer to a board that is accountable to public shareholders — not just the founding promoters.

Suggested Services

- IPO Advisory & Consulting Services in Delhi

- IPO Advisory Services in Mumbai

- SME IPO Advisory Services in Chennai

IPO Eligibility Criteria in India

Not every company can walk into SEBI and file a DRHP. Under Regulation 6 of the ICDR Regulations, a company must qualify through one of two routes before it can pursue a Mainboard IPO.

- Profitability Route (Regulation 6(1)). Net tangible assets of at least ₹3 crore in each of the preceding 3 years, average operating profit of at least ₹15 crore in 3 of the preceding 5 years, and net worth of at least ₹1 crore in each of the preceding 3 years.

- QIB Route (Regulation 6(2)). Companies that don’t meet the profitability track record — including many tech and SaaS businesses — can still list by allocating at least 75% of the issue to Qualified Institutional Buyers, with a full refund if that threshold isn’t met. Zomato and Swiggy both listed through this route.

SME IPOs follow separate, lighter eligibility norms set by NSE Emerge and BSE SME, generally requiring a positive net worth and a shorter operating history than Mainboard listings.

- Also Reads on: SEBI Compliance & DRHP Preparation

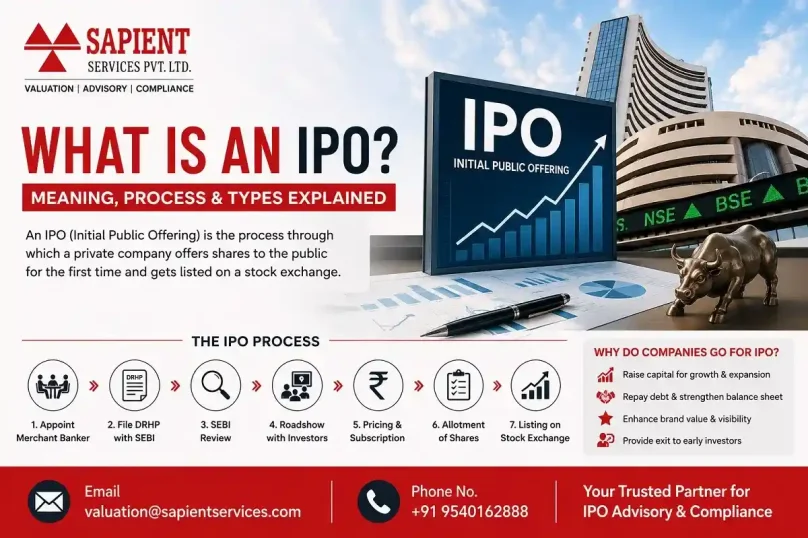

How Does an IPO Work? The Process Step by Step

While every issue has its own timeline, an Indian IPO generally follows the same sequence of steps.

- Appoint a Merchant Banker. The company appoints one or more SEBI-registered merchant bankers (Book Running Lead Managers) along with legal counsel, auditors, and a Registrar to the Issue to structure and administer the offer.

- File the DRHP. The company files a Draft Red Herring Prospectus with SEBI, disclosing its financials, business model, risk factors, litigation history, related-party transactions, promoter holding, and how it plans to use the proceeds.

- SEBI Review. SEBI reviews the DRHP and may raise observations. The company addresses these before getting clearance to proceed — this stage alone can take several weeks.

- Roadshow. Company executives and underwriters meet institutional investors to build interest ahead of the issue opening, typically over one to two weeks.

- Pricing and Subscription. The price is set through the fixed price method or book building, and the issue opens for public subscription, usually for three to four days.

- Allotment. Shares are allotted based on demand in each investor category, and unsuccessful applicants have their blocked funds released.

- Listing. Since December 2023, SEBI requires listing within 3 working days (T+3) of the issue closing — the shares then begin trading on the exchange.

Regulatory Update: SEBI’s board approved easier minimum public offer and dilution norms for very large companies in September 2025. Separately, the SEBI (ICDR) (Third Amendment) Regulations, 2025 (Notification No. SEBI/LAD-NRO/GN/2025/271, effective 30 November 2025) revised the anchor investor framework — expanding permitted anchor investor numbers for larger issues and reserving 40% of the anchor portion for domestic institutions (33.33% mutual funds, 6.67% life insurers and pension funds) for the first time. Recent ICDR amendments have also introduced a mandatory abridged prospectus with a QR code linking to the full offer document. The T+3 listing timeline itself, in place since December 2023, remains unchanged.

Types of IPOs in India

Indian IPOs are priced using one of two methods, and the choice affects how investors bid and how the final price gets discovered.

| Feature | Fixed Price Issue | Book Building Issue |

|---|---|---|

| How the price is set | Company and merchant banker fix one price upfront | A price band is set; final price depends on investor bids |

| Price visibility | Known before the issue opens | Discovered during the bidding process |

| Demand visibility | Known only after the issue closes | Updated daily while bidding is open |

| Used in India today | Rarely, mostly smaller issues | Standard method for most Mainboard and SME IPOs |

Book building has become the default for nearly all sizeable Indian IPOs because it lets market demand, not just the company’s own estimate, determine the final price.

Which Type of IPO Is More Common in India Today?

Almost every Mainboard IPO in India today uses book building, since it lets institutional demand help set a fair price. Fixed price issues are now largely limited to smaller SME IPOs, where the company and merchant banker set one price upfront.

Why Do Companies Launch an IPO?

For a company’s promoters, an IPO is rarely about one single goal — it usually serves several purposes at once.

- Raising growth capital. Fresh capital funds expansion, new facilities, product development, or debt repayment without adding promoter-guaranteed loans.

- Providing an exit or liquidity route. Founders, employees with ESOPs, and early private investors get a regulated route to sell some or all of their holding.

- Building brand credibility. A listed company gains visibility, credibility with customers and lenders, and easier access to future capital raises.

- Enabling acquisitions and ESOPs. Publicly traded shares can be used as currency for acquisitions and as a benchmark for employee stock compensation.

Fresh Issue vs Offer for Sale: Where Does the Money Go?

An IPO can include a Fresh Issue, an Offer for Sale (OFS), or both. In a Fresh Issue, the company creates new shares and the proceeds go into the business. In an OFS, existing shareholders — promoters or early investors — sell their existing shares, and the proceeds go to them, not the company.

Reading this split in the offer document matters: an IPO that is entirely OFS raises no fresh capital for the company itself, even if the headline issue size looks large.

Advantages and Risks of Investing in an IPO

An IPO investment carries a different risk profile from buying an already-listed stock, since the company has little or no public trading history.

- Advantage: Early entry. Investors get in at the same price as everyone else, before the stock develops a trading history — with the potential to benefit from long-term growth.

- Advantage: Liquidity. Listed shares can be bought and sold on the exchange, unlike private company shares which are far harder to transfer.

- Advantage: Transparency. Public companies must disclose financials and material events regularly, giving investors more visibility than a private company offers.

- Risk: Limited track record. With no long trading history, valuing the business is harder, and demand-driven pricing can lead to listing-day volatility in either direction.

- Risk: Uncertain allotment. Heavily oversubscribed IPOs allot shares by computerized lottery, so retail investors often receive only one lot, or nothing at all.

Is Investing in an IPO Safe for First-Time Investors?

An IPO is not inherently riskier or safer than any other equity investment — it simply carries different risks, centered on limited trading history and demand-driven pricing. Reading the RHP’s risk factors section and checking the company’s financial track record matters more than following listing-day hype.

How to Apply for an IPO in India

Retail participation in Indian IPOs runs entirely through the ASBA system, which blocks funds in your bank account rather than debiting them upfront.

- Open a demat account. You need a demat account and a UPI-enabled bank account before an IPO opens for subscription.

- Read the RHP. The Red Herring Prospectus lists the company’s financials, business risks, and how proceeds will be used — read it before bidding.

- Submit your application. Choose your lot size and bid price through your broker’s app or net banking, using the ASBA or UPI route.

- Approve the UPI mandate. Your UPI app will send a mandate request to block the funds — approve it before the bidding window closes, since server delays near the deadline are a common cause of rejected applications.

- Wait for allotment. If the issue is oversubscribed in the retail category, SEBI mandates a computerized lottery so shares are spread across as many unique applicants as possible.

Investor Categories and Bid Limits

SEBI classifies IPO applicants into three categories. Retail Individual Investors (RIIs) can apply up to ₹2 lakh, using UPI mandates capped at ₹5 lakh per transaction. Non-Institutional Investors (NIIs or HNIs) bid above ₹2 lakh through ASBA. Qualified Institutional Buyers (QIBs) are banks, mutual funds, and other institutions bidding in a separate, larger category.

SME IPOs, listed on platforms like NSE Emerge and BSE SME, work differently — the minimum application is raised to about ₹2 lakh (2 lots), and the cut-off price bidding option available in Mainboard IPOs is not offered.

What Is Grey Market Premium (GMP) and Should You Trust It?

GMP is the unofficial premium at which IPO shares trade in an unregulated grey market before listing. It is not published, verified, or endorsed by SEBI or the exchanges — it exists entirely outside the regulated market, and treating it as a pricing signal can be misleading.

A high GMP often signals heavy retail interest, which can actually lower your odds of allotment rather than guarantee listing gains. It can also swing sharply between your application date and listing day, so treat it as one unregulated data point, not a decision-making tool on its own.

Key IPO Terms You Should Know

| Term | What It Means |

|---|---|

| DRHP | Draft Red Herring Prospectus — the preliminary offer document filed with SEBI, minus the final price |

| RHP | Red Herring Prospectus — the final offer document filed once the price is set |

| Price Band | The floor (minimum) and cap (maximum) price range for a book-built issue |

| Book Building | The process of discovering the issue price based on bids from investors |

| Book Running Lead Manager (BRLM) | The SEBI-registered merchant banker managing the issue and, often, guaranteeing a portion of it |

| Registrar to the Issue | The SEBI-registered agency (such as KFin or MUFG Intime) that processes applications and finalizes allotment |

| NSDL / CDSL | India’s two depositories, which hold your shares electronically in your demat account |

| SCSB | Self-Certified Syndicate Bank — the bank authorized to block your funds under ASBA |

| Anchor Investor | A large institutional investor allotted shares a day before the issue opens, at a fixed price; 40% of this portion is reserved for domestic mutual funds, insurers, and pension funds |

| Green Shoe Option | An option letting underwriters sell additional shares if demand is high, to stabilize the price post-listing |

| ASBA | Application Supported by Blocked Amount — your money is blocked, not debited, until allotment |

| GMP | Grey Market Premium — an unofficial, unregulated indicator of listing-day demand that SEBI does not endorse |

IPO vs FPO vs Rights Issue vs Private Placement

An IPO is only one of several ways a company can raise equity capital. The table below shows where it fits among the others.

| Instrument | Who Can Use It | Who Can Invest |

|---|---|---|

| IPO | A private company listing for the first time | General public, via a stock exchange |

| FPO (Follow-on Public Offer) | A company that is already listed, raising more equity | General public, via a stock exchange |

| Rights Issue | A listed company offering new shares to existing shareholders first | Only existing shareholders, in proportion to their holding |

| Private Placement | Any company issuing shares to a select group | A specific set of investors named by the company, not the public |

The distinction matters because each route carries different disclosure requirements, pricing rules, and investor eligibility — an FPO, for instance, follows a lighter disclosure process than an IPO since the company is already listed and reporting publicly.

A Real Scenario From Sapient’s Assignments

From our experience advising companies preparing for a public listing, here is a pattern worth knowing.

Situation: A Delhi NCR-based manufacturing company wanted to time its IPO around a specific quarter, without first confirming how long SEBI’s DRHP observation stage typically takes.

Challenge: The promoters had built a listing timeline around the roadshow and pricing stages alone, without buffer time for SEBI’s review and observation cycle, which can run several weeks depending on query volume.

Sapient’s Approach: We mapped the realistic end-to-end timeline against recent comparable issues and helped the promoters build in contingency time before committing to a listing quarter publicly.

Outcome: The revised timeline avoided a public commitment the company could not control, and the DRHP filing proceeded with realistic milestones built in from the start.

Frequently Asked Questions

Q: What is the full form of IPO?

A: IPO stands for Initial Public Offering — the process through which a private company sells shares to the public for the first time and gets listed on a stock exchange.

Q: What is an IPO in simple terms?

A: An IPO is when a company that was privately owned opens up part of its ownership to the public by selling shares, which then trade freely on a stock exchange like the NSE or BSE.

Q: How long does it take to list on the stock exchange after an IPO closes?

A: SEBI requires listing within 3 working days (T+3) of the issue closing, a rule that has been mandatory since December 2023.

Q: What is the difference between DRHP and RHP?

A: The DRHP (Draft Red Herring Prospectus) is the preliminary offer document filed with SEBI before the price is fixed. The RHP (Red Herring Prospectus) is the final version, filed once the price band or price is confirmed.

Q: What is the minimum amount needed to apply for an IPO?

A: For most Mainboard IPOs, one lot typically costs between ₹10,000 and ₹15,000, though this varies by issue. SME IPOs require a minimum of 2 lots, often ₹2 lakh or more.

Q: What happens if I don’t get IPO allotment?

A: If your application is not allotted shares, the blocked amount in your bank account is released automatically — no money is debited unless shares are actually allotted to you.

Q: What is the difference between fixed price and book building IPOs?

A: In a fixed price IPO, the company sets a single price in advance. In a book building IPO, a price band is set, and the final price is discovered based on investor bids during the subscription period.

Q: Who regulates IPOs in India?

A: The Securities and Exchange Board of India (SEBI) regulates IPOs under its ICDR (Issue of Capital and Disclosure Requirements) Regulations, covering eligibility, disclosure, and pricing norms.

Q: What is an anchor investor in an IPO?

A: An anchor investor is a large institutional investor allotted shares a day before the issue opens to the public, at a price fixed in advance, to help build early confidence in the issue.

Q: Can a loss-making company launch an IPO in India?

A: Yes, subject to SEBI’s ICDR eligibility norms, which offer alternative routes — such as the QIB-heavy route — for companies that do not meet the standard profitability track record.

Q: Is IPO investment guaranteed to be profitable?

A: No. While some IPOs list at a premium to their issue price, others list below it. Past listing performance does not guarantee future returns, and investors should evaluate the company’s fundamentals rather than relying on grey market premium alone.

Q: Can NRIs apply for an IPO in India?

A: Yes, NRIs can apply through the NRI category using their NRE or NRO bank account, typically via the ASBA route, subject to RBI’s FEMA guidelines on repatriation.

Q: What is the cut-off price in an IPO application?

A: The cut-off price option lets retail investors agree to pay whatever final price is discovered within the price band, improving allotment chances. It is not available in SME IPOs.

Q: Do companies get a reserved quota for employees in an IPO?

A: Many companies reserve a portion of the issue for eligible employees, often at a discount to the issue price, disclosed in the DRHP and RHP.

Q: What is the difference between an IPO and an FPO?

A: An IPO is a company’s first-ever sale of shares to the public. An FPO (Follow-on Public Offer) is a subsequent share sale by a company that is already listed on a stock exchange.

Q: Can an IPO be withdrawn or cancelled after filing?

A: Yes. A company can withdraw its DRHP or RHP before allotment due to weak market conditions, insufficient subscription, or its own strategic decision, subject to SEBI’s withdrawal norms.

Why IPO Pricing Isn’t Just Guesswork

The price band behind every book-built IPO is built on a valuation exercise — typically a mix of DCF, comparable company multiples, and the company’s own growth story — conducted by the merchant banker in consultation with the issuer. A mispriced IPO can undersell existing shareholders or leave the stock struggling to hold its price after listing, which is why company valuation work often starts well before the DRHP is filed.

Conclusion

An IPO is far more than a stock market event — it’s the legal and financial process that turns a private company into a public one, governed at every step by SEBI’s disclosure and pricing framework. For companies, it means new capital and public accountability. For investors, it means a chance to participate early, alongside real risks that come with limited trading history.

Whether you are a promoter mapping a listing timeline or an investor evaluating your first public offering, understanding this process end to end — not just the headline IPO date — is what separates an informed decision from a rushed one.

Contact Sapient Services at +91 9540162888 or visit sapientservices.com to speak with our IPO advisory team about preparing your company for a public listing.

- Must Reads on: IPO Investment in India — What Nobody Tells You First