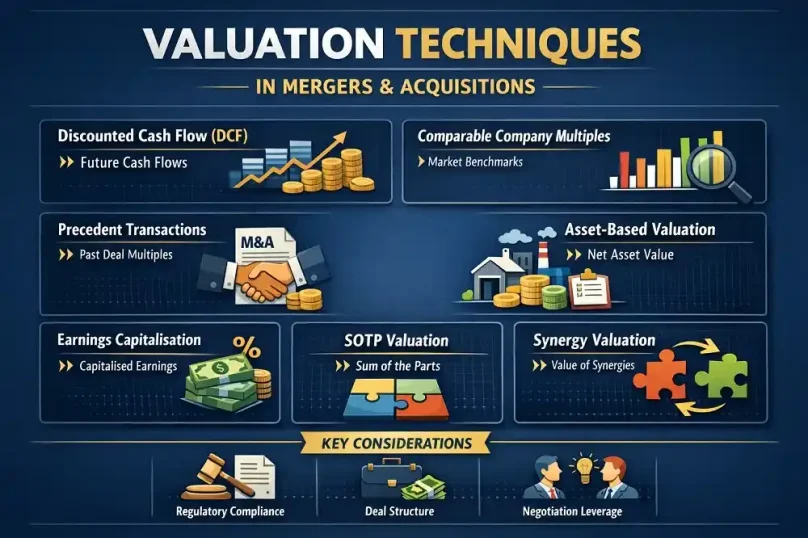

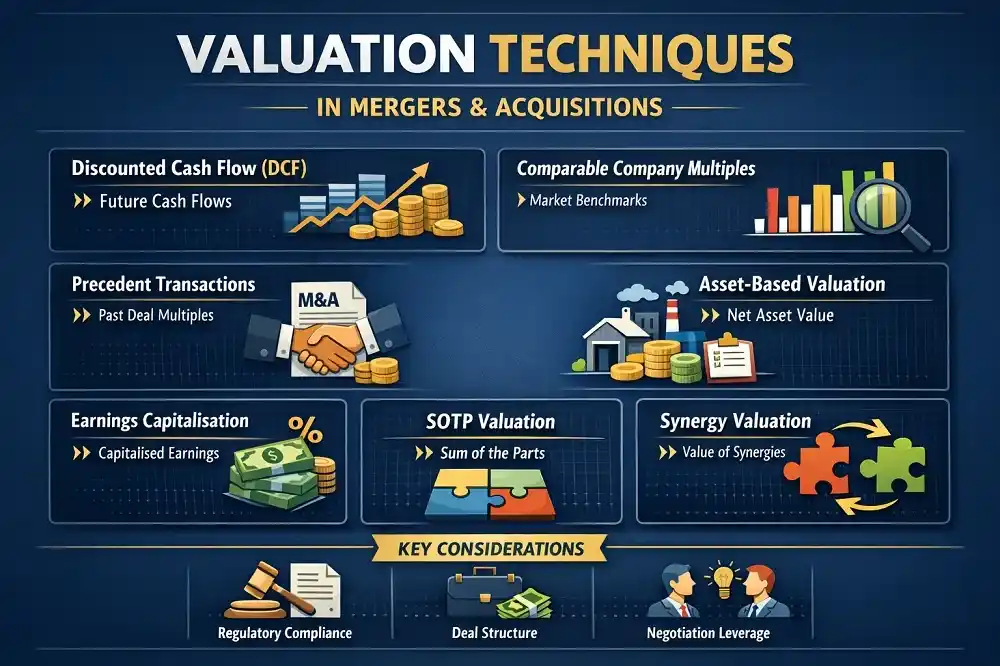

Valuation Techniques in Mergers and Acquisitions

By

By

Valuation sits at the centre of every merger and acquisition, yet it is often misunderstood—even by experienced business owners. In theory, valuation is a financial exercise. In practice, it is a negotiation tool shaped by assumptions, control, risk, regulation, and timing.

In Indian M&A transactions especially, valuation is rarely about arriving at a single “correct” number. It is about establishing a defensible valuation range that can survive scrutiny from buyers, sellers, regulators, lenders, auditors, and sometimes tax authorities.

This article breaks down the most commonly used valuation techniques in M&A, explains when they work, where they fail, and how practitioners actually use them in real transactions—not just in spreadsheets.

Why valuation in M&A is different from routine business valuation

Valuation for internal reporting or fundraising is not the same as valuation for an acquisition.

In M&A:

- Control is changing hands

- Synergies are expected (sometimes unrealistically)

- Risks shift between parties

- Deal structure (cash, equity, earn-outs) matters as much as headline value

In India, additional layers apply:

- Regulatory scrutiny under Companies Act, FEMA, Income Tax Act

- Fair valuation requirements for related-party and cross-border deals

- Valuation reports often reviewed long after the deal closes

This makes method selection as important as the numbers themselves.

Suggested Services

1. Discounted Cash Flow (DCF) Method

What it tries to do

DCF estimates the present value of a business based on expected future cash flows, discounted for risk.

In theory, it is the most “intrinsic” valuation method.

How it is used in Indian M&A

DCF is commonly used:

- In strategic acquisitions

- For growing businesses with predictable cash flows

- In regulatory-driven valuations (fair value opinions, FEMA pricing)

Practical strengths

- Forward-looking, not backward-facing

- Forces clarity on business drivers

- Useful when comparable data is weak

Real-world limitations

This is where DCF often breaks down:

- Cash flow projections are management-driven and optimistic

- Terminal value can contribute 60–80% of valuation

- Small changes in discount rate can swing value materially

In Indian deals, DCF often becomes a justification tool rather than a discovery tool.

When DCF works best

- Mature businesses with stable margins

- Infrastructure, manufacturing, utilities

- When buyer has deep operational visibility

When to be cautious

- Early-stage or loss-making companies

- Businesses dependent on promoter relationships

- Cyclical or policy-sensitive sectors

2. Comparable Company Multiples (Trading Multiples)

What it tries to do

Values a company based on how similar listed companies are priced by the market.

Common multiples:

- EV/EBITDA

- P/E

- EV/Sales

How it is used in practice

This is often the starting point in negotiations.

Buyers use it to anchor expectations. Sellers use it to benchmark upside.

Practical strengths

- Simple and market-linked

- Easy to explain to boards and investors

- Reflects current sentiment

Where it fails in Indian M&A

- Truly comparable listed companies often don’t exist

- Differences in scale, governance, margins are ignored

- Market multiples fluctuate independent of fundamentals

Listed market optimism does not always translate into private deal pricing.

Best use case

- Establishing valuation bands

- Supporting other valuation methods

- Market sanity checks

Not suitable as a standalone method.

3. Precedent Transaction Method

What it tries to do

Looks at valuation multiples paid in past M&A transactions involving similar companies.

Why practitioners like it

- Reflects real acquisition premiums

- Captures control and synergy expectations

- More deal-relevant than trading multiples

Practical challenges

- Limited public data in Indian private deals

- Transaction terms are often undisclosed

- Timing differences distort relevance

Many Indian precedent deals also include:

- Deferred payments

- Earn-outs

- Non-cash considerations

Headline multiples can be misleading if structure is ignored.

Best use case

- Strategic acquisitions

- Sector consolidation plays

- When reliable deal databases are available

4. Asset-Based Valuation

What it tries to do

Values the company based on the fair value of assets minus liabilities.

Variants include:

- Net Asset Value (NAV)

- Adjusted book value

- Replacement cost

Where it is commonly used

- Asset-heavy businesses

- Real estate, manufacturing, holding companies

- Distressed or liquidation scenarios

Strengths

- Balance sheet driven

- Less dependent on projections

- Easier to defend in downside cases

Limitations

- Ignores future earning potential

- Undervalues brands, IP, relationships

- Not suitable for service or tech businesses

In M&A, asset-based valuation usually sets the floor, not the price.

5. Earnings Capitalisation Method

What it tries to do

Capitalises maintainable earnings using a selected capitalisation rate.

Often used as a simplified DCF alternative.

Practical use

- Small to mid-sized businesses

- Where long-term growth is modest

- When forecasting is unreliable

Risks

- Over-simplifies business reality

- Sensitive to capitalisation assumptions

- Less accepted in complex deals

Still useful for:

- Family business acquisitions

- Internal restructurings

- Indicative pricing exercises

6. Sum-of-the-Parts (SOTP) Valuation

What it tries to do

Values each business segment separately and aggregates them.

When it is relevant

- Diversified groups

- Businesses with unrelated verticals

- Conglomerate acquisitions

Practical challenges

- Segment-level financials may be weak

- Allocation of shared costs becomes subjective

- Buyers may discount non-core segments

SOTP is often used in break-up or carve-out scenarios, not straightforward acquisitions.

7. Valuation in Synergy-Driven Deals

Synergies are where theory and reality diverge sharply.

Common synergy assumptions:

- Cost savings

- Cross-selling

- Procurement efficiencies

- Tax optimisation

Practical reality

- Synergies are buyer-specific

- Integration risk is high

- Cultural and operational friction erodes value

Experienced buyers often:

- Value the target on a standalone basis

- Pay for only a portion of expected synergies

Overpaying for theoretical synergies is one of the most common causes of value destruction.

Regulatory and compliance considerations in India

Valuation in Indian M&A cannot ignore compliance.

Common regulatory touchpoints:

- Companies Act (registered valuer requirements)

- FEMA pricing guidelines

- Income tax scrutiny (especially in related-party deals)

- SEBI regulations for listed entities

Valuation reports often need to be:

- Defensible

- Well-documented

- Methodologically consistent

A technically sound valuation that ignores regulatory expectations can still create post-deal issues.

Choosing the right valuation approach: practical guidance

No serious M&A deal relies on one method.

In practice:

- 2–4 methods are applied

- One becomes the primary reference

- Others provide support and boundaries

Suitable combinations

- DCF + trading multiples

- Precedent transactions + DCF

- Asset-based + earnings capitalisation

The final price is influenced by:

- Negotiating leverage

- Competitive tension

- Strategic fit

- Timing and market sentiment

Valuation sets the battlefield. Negotiation decides the outcome.

Who this information is most useful for

- Business owners considering a sale or merger

- CFOs and finance heads preparing for transactions

- Strategic buyers evaluating acquisition targets

- Investors assessing fair value expectations

Who should be cautious

- Early-stage founders expecting valuation formulas to dictate price

- Sellers relying only on headline multiples

- Buyers assuming spreadsheets replace integration planning

Frequently Asked Questions (FAQs)

1. Is DCF the most accurate valuation method in M&A?

No. DCF is sensitive to assumptions and works best alongside other methods.

2. Why do buyers and sellers arrive at different valuations?

Because assumptions on growth, risk, and synergies differ.

3. Are valuation multiples from listed companies reliable?

They are indicative, not decisive, especially for private companies.

4. How important are synergies in valuation?

They matter, but overpaying for unproven synergies is risky.

5. Does valuation decide the final deal price?

Not always. Negotiation power and deal structure play major roles.

6. Can valuation change after due diligence?

Yes. Findings often lead to price adjustments or restructuring.

7. Are asset-based valuations still relevant?

Yes, especially for asset-heavy or distressed businesses.

8. How do earn-outs affect valuation?

They shift risk and bridge valuation gaps between parties.

9. Is regulatory valuation different from commercial valuation?

Often yes. Regulatory focus is fairness, not strategic value.

10. Should promoters rely on one valuation report?

No. Multiple perspectives improve decision quality.