What is Insurance Advisory Service

By

By

Most business owners treat insurance like a routine expense. They buy a policy, pay the premium every year, and hope they never have to use it. But that approach leaves a lot of businesses either paying for coverage they don’t need — or exposed in ways they haven’t considered.

This is exactly what insurance advisory service is designed to fix. It’s not about selling you one more policy. It’s about making sure the coverage you already have is actually doing its job — and filling in the gaps where it isn’t. If you’re looking for expert guidance, explore our insurance advisory services in Delhi, India designed for businesses across industries.

In 2026, businesses are dealing with a wider range of risks than before — cyber threats, stricter regulations, rising claim costs, and supply chain disruptions. A proper insurance advisory engagement helps businesses respond to these challenges without overpaying or leaving critical areas unprotected.

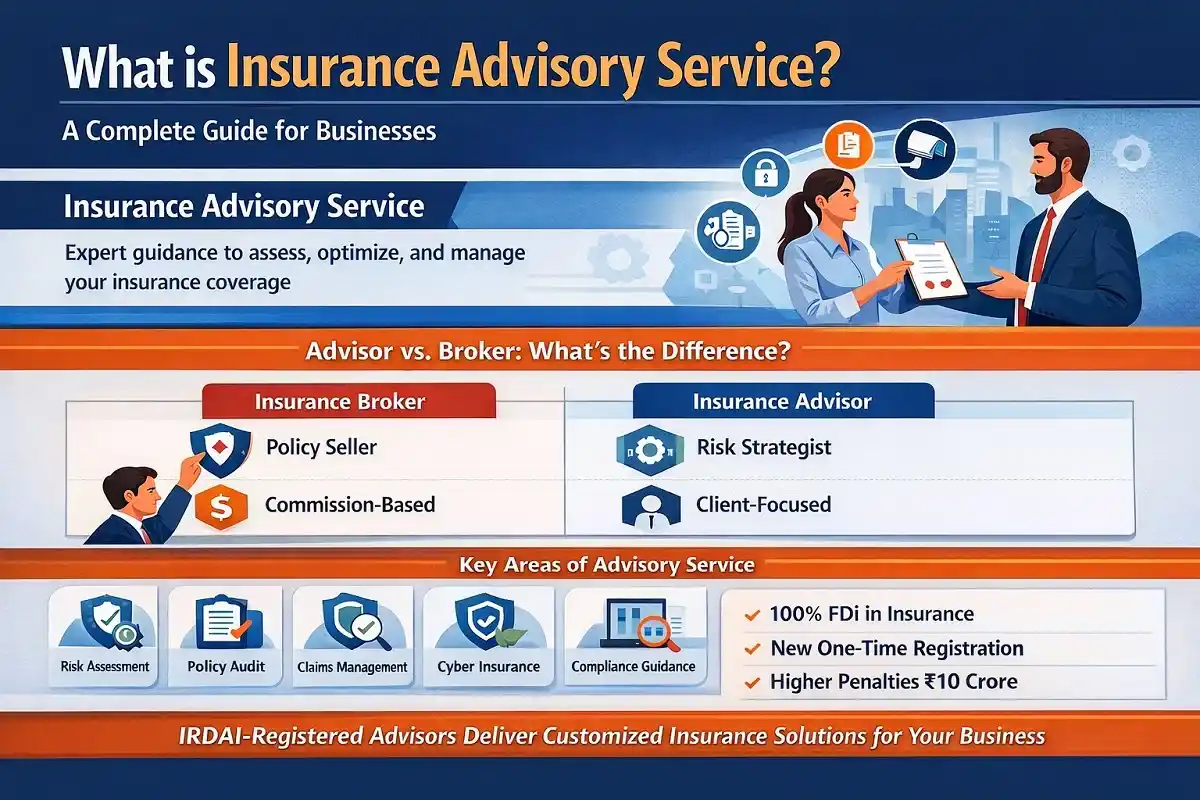

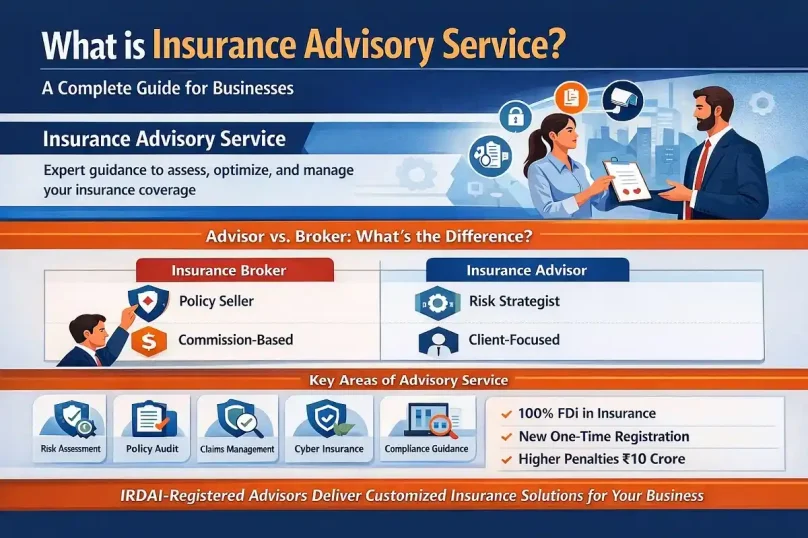

What is Insurance Advisory Service?

Insurance advisory service is a professional service where trained experts help businesses evaluate, design, and manage their insurance programs. The focus is on your specific business — your risks, your industry, your budget — not a generic policy from a brochure.

The key difference from just buying insurance is this: an advisor works entirely for you. They review what you have, compare it against what your business actually needs, identify what’s missing or redundant, and help you build a plan that makes sense for your situation.

According to B.F. Saul Insurance, an established U.S.-based advisory firm, insurance advisors contact multiple carriers on a client’s behalf, evaluate and negotiate different options, and sometimes combine coverages from more than one insurer — which is often the only way to get the full protection a business actually needs.

Think of it this way — a policy is a product you buy. An advisory service is a strategy built around your business.

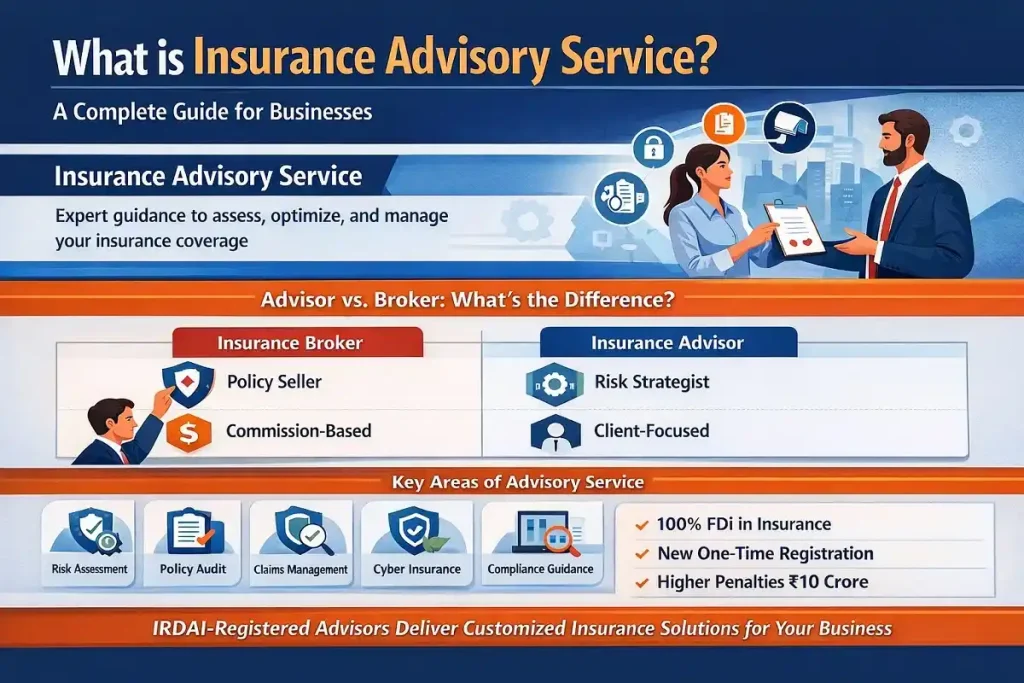

Insurance Advisor vs. Insurance Broker — What’s the Difference?

These two terms are often used as if they mean the same thing. They don’t. Here’s a clear breakdown:

| Parameter | Insurance Broker | Insurance Advisor |

| Primary Role | Sells and renews policies | Manages the full risk strategy |

| Working Style | Transaction-based | Ongoing, relationship-driven |

| How They’re Paid | Commission from insurer | Fee from client (or hybrid) |

| Engagement Period | Mainly at renewal time | Throughout the year |

| Who They Work For | Technically for the client, but commission-driven | Fully for the client — no insurer ties |

The real difference is transactional versus consultative. A broker’s job is to help you buy and renew insurance products — that’s where their engagement typically begins and ends. An advisor, on the other hand, manages your insurance program as a whole. They look at whether your coverage is working for you throughout the year, not just at renewal.

Both have their place. But if your business has grown, has employees, operates in multiple locations, or deals with data and clients — a dedicated advisor tends to deliver more value over time.

Why Businesses Need Insurance Advisory Service

1. Finding Coverage Gaps Before a Claim Reveals Them

Most businesses buy a standard policy without checking whether it actually matches their exposure. A manufacturing company without machinery breakdown coverage, or a tech firm without cyber liability insurance, is one incident away from a significant financial problem.

BDO Advisory, a major global accounting and advisory firm, notes that a well-structured insurance program must take an integrated view of risk across all business functions — not just the most obvious ones. Gaps exist in almost every program that hasn’t been properly reviewed.

2. Cutting Down on Wasted Premiums

Overpaying for insurance is just as common as underinsurance. Many businesses carry overlapping coverage across policies — paying for protection twice in some areas while leaving other areas completely exposed. An advisor benchmarks your program, cuts what’s redundant, and finds better pricing where possible.

3. Claims Support When It Matters Most

Filing a claim and actually getting a fair payout are two different things. Because advisors work independently — not for any insurer — they can step in as your advocate. They help with documentation, push back on undervalued claims, and negotiate directly with the insurer on your behalf.

B.F. Saul Insurance’s published guidance confirms that advisors can serve as a client’s claims advocate, helping achieve the best outcome if a covered loss occurs.

4. Keeping Up with Regulatory Changes

In India, the regulatory environment changed significantly in late 2025. The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Bill, 2025 — passed by both houses of Parliament in December 2025 — brought in 100% FDI for insurance companies, a simpler one-time registration system for intermediaries, and much higher penalties for violations (up from ₹1 crore to ₹10 crore). An advisor tracks these shifts and makes sure your business is on the right side of them.

5. Coverage That Grows With Your Business

Taking on new employees, expanding to a new city, launching a new product — each of these changes your risk profile. A good advisor reviews your coverage whenever something material changes, not just when the renewal notice arrives.

What Insurance Advisory Service Includes

The scope varies depending on the firm and the engagement, but these are the core services most businesses can expect:

- Risk Assessment — A full review of your business operations, industry-specific exposures, financial obligations, and legal requirements

- Policy Audit — Every existing policy is reviewed for adequacy, exclusions, coverage gaps, and whether it still fits your current business

- Insurance Gap Analysis — Pinpoints areas where your business is unprotected and a claim would fall outside your current coverage

- Market Benchmarking — Your program is compared against industry peers to check for overpricing or underinsurance

- Claims Management — Guides you on documentation, timing, and negotiation to get the best possible outcome from a claim

- Regulatory & Compliance Advisory — Keeps your coverage aligned with IRDAI regulations, labor laws, and sector-specific compliance requirements

- Third-Party Risk Transfer — Reviews contracts with vendors and suppliers to identify where insurance obligations should be placed on other parties

Key Types of Insurance Coverage Businesses Should Know

An advisor doesn’t push one product — they build a mix based on your industry, structure, and actual risk exposure. The following are the most common coverage types relevant to businesses:

| Insurance Type | Who Needs It | What It Covers |

| General Liability | All businesses | Third-party bodily injury, property damage, advertising injury |

| Professional Liability (E&O) | Consultants, IT firms, service providers | Negligence claims, errors, failure to deliver a promised service |

| Commercial Property | Any business with physical assets | Fire, theft, vandalism, certain weather events |

| Cyber Insurance | IT, fintech, e-commerce, healthcare | Data breaches, ransomware, business email compromise |

| Workers’ Compensation | Any business with employees | Medical costs and lost wages from on-the-job injury or illness |

| D&O Insurance | Companies with a board or directors | Personal liability of directors from business decisions |

| Business Interruption | All businesses | Lost revenue and fixed costs when operations are forced to stop |

| Key Person Insurance | SMEs, startups | Financial loss if a critical person dies or becomes disabled |

A logistics company’s needs look very different from a software firm’s or a construction company’s. That’s the whole point — there’s no standard program that works for everyone. The coverage mix has to reflect how your business actually operates.

India-Specific Context: IRDAI and the Regulatory Framework

For businesses operating in India, insurance advisory and intermediary activity is regulated by the Insurance Regulatory and Development Authority of India (IRDAI) — a statutory body established under the IRDAI Act, 1999 and operating under the Ministry of Finance.

IRDAI’s mandate covers protecting policyholders, licensing intermediaries, regulating premium rates, and ensuring insurers maintain adequate solvency margins. Any person or firm providing insurance advisory or broking services in India must be registered with IRDAI — no exceptions.

Key Changes in 2025–2026

- 100% FDI now permitted — Foreign companies can fully own Indian insurance entities under the Insurance Amendment Bill, 2025

- One-time registration for intermediaries — Replaces fixed-term renewal; advisors now get permanent registration subject to annual compliance and fee payment

- Higher penalties for violations — Maximum penalty raised from ₹1 crore to ₹10 crore under the amended Insurance Act

- Insurance for All by 2047 — IRDAI’s national target to ensure every Indian citizen and business has appropriate coverage by India’s centenary year

- Fraud Monitoring Framework — Effective April 1, 2026 — expanded to cover distribution channels, mandates Fraud Monitoring Committees in all insurers

Insurance brokers in India operate under the IRDAI (Insurance Broker) Regulations, 2018. Their role is defined as advisory, fiduciary, and compliance-driven — going well beyond just finding and selling policies. Direct brokers must maintain mandatory professional indemnity insurance with minimum coverage of ₹1 crore, and composite brokers at ₹10 crore.

How the Insurance Advisory Process Works — Step by Step

| Step | Stage | What Actually Happens |

| 1 | Business Assessment | Advisor learns your industry, business model, size, and existing coverage |

| 2 | Risk Profiling | Your specific vulnerabilities are mapped — operational, financial, legal, reputational |

| 3 | Gap Analysis | Gaps between what you have and what you actually need are identified |

| 4 | Market Research | Multiple insurers are compared; the advisor negotiates terms on your behalf |

| 5 | Policy Structuring | A coverage plan is built around your budget, industry norms, and risk appetite |

| 6 | Implementation | Policies are executed, paperwork completed, key staff briefed |

| 7 | Ongoing Review | Coverage is revisited when the business grows, changes, or regulations shift |

What to Look for When Choosing an Insurance Advisor

Not every advisory firm delivers the same quality of work. Here’s what to actually check before you bring someone on:

- IRDAI Registration — Any legitimate insurance intermediary operating in India must be IRDAI-registered. You can verify this directly at irdai.gov.in

- Fee Structure Clarity — Understand exactly how the advisor gets paid. Fee-only advisors (no insurer commission) tend to give more objective advice because they have no financial reason to favor one insurer over another

- Relevant Industry Experience — A firm that works mainly with manufacturing clients may not understand the specific risks of a healthcare business or a tech startup. Ask for industry-specific references

- Claims Track Record — Ask how they’ve handled past claims for clients. The real test of any advisor is how they perform when a loss actually happens

- Independent Ownership — B.F. Saul Insurance’s research notes that private equity-backed advisory firms can face conflicts of interest due to aggressive financial targets. An independently owned firm is more likely to prioritize your interests over internal profitability goals

- Plain Language Communication — A good advisor explains what your policy actually covers — and doesn’t cover — in clear terms. If they can’t explain an exclusion simply, that’s a warning sign

Common Insurance Mistakes Businesses Make

These show up across industries and business sizes. Most of them are avoidable with a proper annual review.

- Underinsurance — Property values and liability exposure tend to grow over time, but the insured value often doesn’t get updated. When a claim hits, the gap becomes a real problem

- Buying the Wrong Type of Coverage — General liability and professional liability are not the same thing. Businesses in service industries often carry the wrong one and only find out when a claim is rejected

- Renewing Without Reviewing — Renewing the same policy every year without checking whether it still fits the business is one of the most widespread habits — and one of the most costly

- Late Claims Reporting — Not reporting incidents on time is one of the most common reasons claims get denied or reduced. Most policies have strict reporting windows

- Skipping Employee Benefits Coverage — Many SMEs don’t set up group health or term life cover, which creates compliance issues and makes it harder to retain good employees

- Underestimating Cyber Exposure — India’s rapid growth in digital payments, cloud storage, and remote work has made cyber incidents a real risk even for small and mid-size businesses. It’s not just a concern for large enterprises

How Much Does Insurance Advisory Service Cost?

Cost depends on the scope of work, the size and complexity of the business, and the engagement model the advisor uses. Here are the four most common structures:

| Model | How It Works | Best For |

| Retainer-Based | Fixed monthly or annual fee | Large businesses with ongoing, complex needs |

| Project-Based | One-time fee for a specific task | Policy audits, one-off reviews, claims support |

| Commission-Based | Advisor earns from the insurer | SMEs with straightforward coverage needs |

| Fee + Commission (Hybrid) | Combination of both | Mid-size businesses |

The fee-only model is the cleanest from an objectivity standpoint — the advisor’s income has no connection to which insurer or product you end up choosing. As noted in research from DeshCap, an independent advisory firm, an advisor’s compensation should be structured so they remain impartial in their technical advice.

For most SMEs and mid-market businesses, the cost of a proper advisory engagement is recovered fairly quickly through more appropriate coverage, removed duplications, and better claim outcomes.

Where Insurance Advisory Is Heading in 2026

The commercial insurance market in 2026 is more stable than it was in 2022–2023, but businesses still face real pressure. Inflation in construction and medical costs, skilled labor shortages, climate-related property losses, and changing liability standards are all pushing claim severity higher.

Cyber insurance has entered a new pricing phase. After a brief softening in 2024–2025, rates are rising again. AI-driven threats — deepfake fraud, voice cloning, machine-generated phishing attacks — have made cyber underwriting more cautious and more specific. The B.F. Saul Insurance 2026 Market Report notes that businesses with weak internal controls face real difficulty getting adequate cyber coverage at competitive rates.

On the technology side, Accenture’s published research shows that senior underwriting executives expect AI adoption in insurance to grow from 14% to around 70% within three years. But the report also notes that 81% believe this will create new roles — not replace advisors. The human side of insurance advisory — understanding a client’s business, reading a claim situation, negotiating with underwriters — is not something a platform automates easily.

For businesses, the practical takeaway is straightforward: get your program reviewed by someone who understands your industry. Don’t wait for a claim to find out what your policy doesn’t cover.

Frequently Asked Questions

Q1. What is the difference between an insurance advisor and an insurance broker?

A broker primarily helps you find and purchase insurance policies, earning a commission from the insurer. An advisor takes a wider role — reviewing your full risk picture, auditing existing policies, filling gaps, and supporting claims. Advisors typically charge a fee and have no financial reason to favor a specific insurer.

Q2. Do small businesses really need an insurance advisor?

Yes — and arguably they benefit more than large businesses. A small company has less financial cushion to absorb a coverage gap or a denied claim. An advisor helps make sure the budget is going toward coverage that actually protects the business, not just filling a policy checklist.

Q3. Does an insurance advisor in India need to be IRDAI registered?

Yes. Under the IRDAI Act, 1999, all insurance intermediaries operating in India — including brokers and advisors — must be registered with IRDAI. You can check the registration status of any intermediary directly at irdai.gov.in.

Q4. What does cyber insurance cover for businesses?

Cyber insurance typically covers costs from data breaches, ransomware attacks, business email compromise, and regulatory notifications. Coverage usually includes incident response, legal fees, and income lost during downtime. With digital payment volumes and cloud usage growing rapidly in India, this has become relevant for businesses across sectors — not just large tech firms.

Q5. How is an insurance advisor typically compensated?

There are three main models: fee-based (client pays directly, no insurer commission), commission-based (advisor earns from the insurer on policies placed), and a hybrid of both. Fee-based arrangements tend to produce more objective advice because the advisor’s income isn’t tied to which products or insurers you end up with.

Q6. What does a policy audit actually involve?

An advisor goes through every existing policy — checking whether coverage limits match your current exposure, flagging exclusions that could affect valid claims, identifying duplicate coverage across policies, and benchmarking your premiums against market rates. The result is a clear picture of where you’re adequately covered, where you’re paying for things you don’t need, and where there are real gaps.

Q7. What does business interruption insurance actually cover?

When an insured event — fire, flood, equipment breakdown — forces a business to stop or significantly reduce operations, business interruption insurance covers lost revenue and ongoing fixed costs like rent, staff salaries, and loan repayments during the recovery period. Many SMEs skip this coverage and discover its value only after a loss.

Q8. What is D&O insurance and who needs it?

Directors and Officers insurance covers the personal liability of directors and senior management for decisions made in their professional capacity. It’s important for companies with a board of directors, investor-backed startups, listed entities, and any business where leadership decisions are regularly scrutinized or challenged.

Q9. When is the right time to engage an insurance advisory service?

Good trigger points include: business expansion, a significant change in headcount, new product launches, a funding round, or any time your operations change materially. Annual policy renewals are also a natural time for a review. The ideal time is before you actually need the coverage — not after an incident reveals what’s missing.

Q10. Can an insurance advisor help after a claim has already been filed?

Yes. Claims advocacy is a core part of what advisors do. If you feel a filed claim is being undervalued, delayed without valid reason, or denied unfairly, an advisor can review the documentation, challenge the insurer’s position, and negotiate a better settlement on your behalf.

Final Thoughts

Insurance advisory service isn’t something reserved for large corporations with dedicated risk teams. It’s a practical tool for any business that wants to stop guessing whether its coverage is adequate.

The real value shows up in two places: before a loss, when a proper program prevents you from being caught exposed — and after one, when an advisor makes sure you get a fair outcome from your claim.

If you haven’t had your policies reviewed in the last two years, that’s probably the most useful place to start. Find an IRDAI-registered advisor with experience in your industry, get an honest audit of what you have, and make adjustments based on how your business actually operates today.

Disclaimer: This article is for informational purposes only and does not constitute insurance, legal, or financial advice. For decisions specific to your business, consult a licensed, IRDAI-registered professional. All regulatory references are based on publicly available information as of April 2026.