AI Startup Valuation in India: Revenue Multiples & Investor Trends

By

By

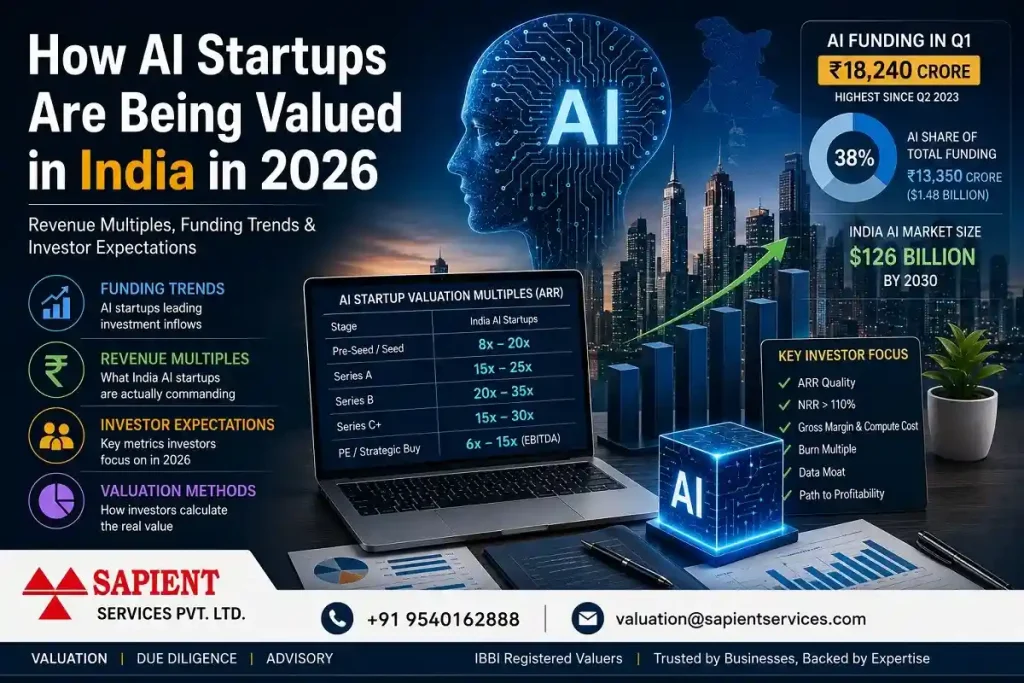

In Q1 2026, Indian AI startups raised $1.48 billion — approximately 38% of India’s total $3.9 billion in startup funding that quarter (Inc42/ipocentral.in data). AI startup valuation in India has become one of the most discussed — and most misunderstood — topics in the Indian investment community. The headline deals are striking: Neysa raised $1.2 billion in February 2026 in a Blackstone-led deal ($600M equity + $600M debt), making it India’s largest AI infrastructure investment. Krutrim became India’s first AI unicorn at a $1 billion valuation on a $50 million raise.

But for a founder or investor trying to understand what an Indian AI company is actually worth — headline funding totals tell you very little. The more important questions are: what revenue multiple is being applied, which metrics drive or destroy the valuation, and how does India differ from global AI valuation benchmarks?

This article answers all three — based on verified Q1 2026 funding data, current valuation benchmarks, and what sophisticated investors in India are actually requiring before writing a cheque.

|

Need an Independent AI Startup Valuation? Contact Sapient Services → +91 9540162888 | valuation@sapientservices.com |

India’s AI Funding Landscape — What the 2026 Data Actually Shows

India’s startup ecosystem raised approximately $10.5 billion in 2025 — a 17% decline from 2024, with deal count falling 39% to 1,518 transactions (Tracxn). The decline was not uniform: seed-stage funding fell 30%; late-stage rounds shrank 13% as investors prioritised businesses with visible exit pathways.

Against this broad contraction, AI stood out sharply. Q1 2026 saw $1.48 billion flow into Indian AI and AI-adjacent companies — 38% of total Q1 2026 startup funding of $3.9 billion. The India AI market is projected to reach $126 billion by 2030 (NASSCOM/IDC). India now hosts over 4,500 AI startups, with 482 funded companies having collectively raised $3.4 billion in VC and PE capital (Inc42 data).

One comparison illustrates the India-global gap: globally, AI attracted nearly $202 billion in venture funding in 2025 (Bain & Company), with US AI startups alone absorbing $159 billion. India’s entire startup ecosystem raised $10.5 billion across all sectors. The India AI opportunity is real — but it is being funded at a different pace, with a different risk framework, than prevails in Silicon Valley.

| Indian AI-focused startups have attracted valuation premiums relative to comparable non-AI peers — but only when the AI application drives measurable business outcomes, not when it is a positioning layer on an existing product. |

AI Company Valuation Methods India — What Revenue Multiples Are Being Applied

Globally, AI startups traded at 25–30x EV/Revenue multiples in 2025–26, compared to approximately 6x for public SaaS companies (CB Insights). Premium companies with strong ARR retention and infrastructure moats reached 50–100x. At seed stage, median pre-money valuations for AI startups stood at $17.9 million — approximately 42% higher than non-AI peers at the same stage.

In India, the multiple range is more compressed. The global 25–30x applies primarily to companies with significant export revenue or those evaluated by global investors. For Indian AI companies primarily serving the domestic market, realistic revenue multiples in 2026 look like this:

| Stage | India AI — Typical Valuation Multiple | Key Driver in India Context |

|---|---|---|

| Pre-Seed / Seed | 8x–20x ARR (if any); often team + TAM based | Founder pedigree, problem specificity, pilot traction, proprietary data access |

| Series A | 15x–25x ARR for B2B SaaS with AI core | ARR growth rate, NRR above 110%, enterprise client count, gross margin quality |

| Series B | 20x–35x ARR (high growth); 10x–18x (moderate growth) | Burn multiple efficiency, path to profitability, ARR per headcount |

| Series C+ | 15x–30x ARR; increasingly EBITDA-adjacent | Competitive moat, international revenue, IPO thesis clarity |

| PE / Strategic buy | 6x–15x EBITDA or 8x–12x Revenue for mature companies | Proven margins, customer lock-in, integration complexity |

One critical India-specific distinction: investors are separating ‘AI-native’ companies — where the AI model is the core product — from ‘AI-augmented’ businesses — where AI is a productivity feature on an existing service. The former command genuine AI multiples. The latter are valued closer to their underlying business model, with a modest premium.

Krutrim illustrates the India AI premium at its most extreme: $1 billion valuation on $50 million raised — before meaningful commercial revenue — on the strength of a large language model for Indian languages. That kind of pre-revenue premium is reserved for foundational AI infrastructure, not AI-enabled services.

|

Sapient Services provides IBBI-registered AI startup valuation for fundraising, ESOP pricing, FEMA compliance, and M&A. Call +91 9540162888 |

Five Metrics That Drive AI Startup Valuation in India

Revenue multiples are the output of valuation, not the input. The metrics investors examine before arriving at a multiple have shifted significantly since 2022, when growth-at-any-cost was sufficient to raise a round.

1. ARR Quality — Not Just ARR Quantity

Investors dissect annual recurring revenue rather than accept it at face value. Annual contract value, multi-year versus month-to-month commitments, usage-based versus seat-based pricing, and auto-renewal rates are all scrutinised. A company with ₹10 crore ARR on 3-year enterprise contracts is valued materially differently from one with identical ARR on monthly auto-renew agreements with high churn risk.

2. Net Revenue Retention (NRR)

NRR — revenue retained from existing customers including expansions, minus churn — is widely regarded as one of the strongest indicators of sustainable AI business value. An NRR above 120% commands premium multiples. In India, B2B AI companies with NRR above 110% are considered high quality; below 90% triggers significant discounts regardless of growth rate.

3. Gross Margin — Especially Compute Cost

This is where Indian AI companies frequently face valuation haircuts founders don’t anticipate. AI inference costs — GPU compute, API calls — sit in cost of goods sold, directly reducing gross margin. A company reporting 80% gross margin is valued very differently from one reporting 40% after compute costs. Investors now explicitly model compute cost as a percentage of revenue and project how it scales.

OpenAI’s numbers illustrate the compute cost problem at scale: the company spent approximately $5.6 billion on compute in 2024 against $3.7 billion in revenue (multiple verified sources including Epoch AI and Reuters). By 2025, OpenAI’s revenue reached $13 billion (Reuters confirmed) while compute costs scaled proportionally. Indian AI startups relying on third-party LLM APIs face this ratio scrutiny particularly hard — their compute costs are variable and vendor-dependent.

4. Burn Multiple

Burn multiple — net burn divided by net new ARR — measures how much capital is consumed for every rupee of new annual recurring revenue added. A burn multiple below 1.5x is considered efficient in 2026; above 2x raises questions; above 3x requires a compelling narrative. For Indian AI startups, where capital efficiency has always been a competitive strength, investors expect lower burn multiples than US counterparts at equivalent stages.

5. Proprietary Data and Model Defensibility

The most defensible AI companies in 2026 are those with proprietary data assets that make their models progressively more accurate — not those using the best third-party models. Indian AI companies with access to India-specific datasets — regional language corpora, healthcare records, agricultural data, financial transaction patterns — command premiums that purely API-wrapper businesses do not.

What Indian Investors Are Prioritising — 2026 Shift

Accel India remains the most active investor in Indian AI by deal count. Peak XV Partners (formerly Sequoia India), Lightspeed India, and Blume Ventures are the other most active domestic VC funds. Their observed investment criteria in 2026 have shifted significantly from 2022:

- Enterprise-first over consumer: Consumer AI in India faces low willingness to pay and high CAC. Enterprise and B2B AI with clear ROI metrics — cost reduction, productivity gains — is where capital is concentrating.

- Vertical depth over horizontal breadth: AI companies building deep solutions for a single vertical (healthcare, agriculture, fintech compliance, legal documents) command higher multiples than horizontal platforms at the same ARR, because competitive moat is demonstrably deeper.

- India-specific language and context: Companies building for India’s linguistic diversity — Sarvam AI’s multilingual LLM (backed by Lightspeed, Peak XV, Khosla in a $53M Series A), Krutrim’s 13-language model — receive strategic premium from investors who believe India-specific AI has a structural advantage over global models.

- Path to profitability, not just growth: The 2025 reset in India startup valuations has permanently shifted investor appetite toward companies with visible EBITDA timelines.

- International revenue as a signal: Qure.ai (3,000+ sites globally) demonstrates that Indian AI companies with export revenue are valued at global multiples, not domestic ones. A startup generating 30–40% revenue from US or MENA enterprise clients commands significant premium over domestic-only peers.

|

The question investors in India are asking in 2026 is not ‘how fast is this company growing?’ It is: ‘what will this company look like at ₹100 crore ARR, and is the gross margin structure sustainable at that scale?’ |

How IBBI Registered Valuers Value AI Startups in India

For regulatory, compliance, and transaction purposes in India, AI startup valuation follows frameworks governed by the Companies Act 2013, Income Tax Act 2025, and FEMA/SEBI guidelines — distinct from VC term sheet negotiations. An IBBI-registered valuer provides a formal business appraisal that is defensible before regulators, tax authorities, and courts.

Three methods are used in practice for AI startup fair value assessment:

ARR Multiple / Comparable Company Method (CCM)

The valuer identifies comparable listed companies and recent private transaction multiples — adjusted for the Indian AI company’s growth rate, gross margin profile, and NRR. A liquidity discount of 20–35% is typically applied for private company status. This is the most common method for B2B SaaS and subscription AI businesses from Series A onwards.

Discounted Cash Flow (DCF) with Scenario Analysis

Increasingly used for later-stage AI companies where cash flows are visible. The distinctive challenge for AI companies: ‘displacement risk’ — the probability that open-source models or platform providers will commoditise the core technology. Valuers model probability-weighted scenarios: base case (moat maintained), bear case (partial commoditisation), and stress case (technology disrupted). The weighted average determines the fair value conclusion.

Venture Capital Method (for Early Stage)

For pre-revenue or early-revenue AI startups, the VC method works backward from a projected exit value — using comparable acquisition multiples or IPO valuations — and discounts back to the present at a risk-adjusted rate (typically 30–60% for Indian AI startups at Series A and below). This method is used for ESOP valuation and FEMA compliance for cross-border AI company investments.

Rule 11UA of the Income Tax Rules governs the valuation methodology for unlisted equity shares in India — used for FEMA pricing in AI company acquisitions and ESOP fair market value determination. Non-compliance creates tax exposure for both the company and its shareholders.

Three Valuation Risks Specific to Indian AI Companies

1. LLM API Dependency

Startups building on OpenAI, Gemini, or Anthropic APIs face a structural risk: if the underlying provider changes pricing, restricts access, or launches a competing product, the startup’s competitive position is threatened overnight. Investors apply a dependency discount for companies where more than 40–50% of core product functionality relies on a single third-party model.

2. Government and Regulated Sector Revenue Concentration

Several Indian AI startups have significant revenue from government contracts — AI for land records, healthcare under Ayushman Bharat, agricultural advisory. Government revenue is valuable but volatile: procurement timelines shift, budget cycles change, and a single policy decision can affect an entire revenue stream. Investors haircut government-concentrated ARR when calculating enterprise value.

3. Talent and Key-Person Risk

India’s AI talent shortage is real. A 100-person AI company with 15 ML engineers is structurally fragile — the departure of 3–4 key researchers can materially affect product development and investor confidence. Investors examine ESOP structure, bench depth, and whether the company has built ML infrastructure that reduces key-person dependency before assigning premium multiples.

Frequently Asked Questions

Q1. How are AI startups valued in India in 2026?

AI startup valuation in India uses three primary methods: the ARR Multiple / Comparable Company Method (most common for B2B SaaS from Series A onwards), DCF with scenario analysis (for later-stage with visible cash flows), and the Venture Capital Method (for early-stage and ESOP pricing). The method depends on stage, revenue visibility, and the purpose of the valuation — fundraising, M&A, FEMA compliance, or ESOP.

Q2. What revenue multiple do Indian AI startups command in 2026?

Indian AI startups typically command 8x–20x ARR at seed/pre-Series A, 15x–25x at Series A, and 20x–35x at Series B for high-growth companies. These are lower than global multiples (25–30x+) because most Indian AI companies primarily serve the domestic market. Companies with significant international revenue or infrastructure AI moats command higher multiples comparable to global benchmarks.

Q3. What is NRR and why does it drive AI startup valuation?

NRR (Net Revenue Retention) measures the percentage of revenue retained from existing customers including expansions, minus churn. An NRR above 120% indicates existing customers are expanding faster than new customers churn — the clearest sign of product-market fit and value creation. Indian B2B AI companies with NRR above 110% command premium multiples; below 90% triggers significant valuation discounts regardless of ARR growth rate.

Q4. What is burn multiple and how does it affect AI company valuation?

Burn multiple = net cash burn divided by net new ARR. It measures capital efficiency — how much is spent to generate each rupee of new recurring revenue. A burn multiple below 1.5x is considered efficient in India’s 2026 funding environment. Above 2x, investors require a compelling narrative. AI companies with high compute costs and low margins frequently have poor burn multiples, which compress valuation even when ARR growth is strong.

Q5. How is AI startup valuation for fundraising different from a regulatory valuation?

A fundraising valuation is a negotiated outcome between the company and the investor — it reflects expectations, not just financial metrics. A regulatory valuation (for FEMA compliance, ESOP pricing, M&A, or tax purposes) must be prepared by an IBBI-registered valuer using documented methods under Rule 11UA of the Income Tax Rules or SEBI/FEMA guidelines. The two can differ significantly — the regulatory valuation must be defensible before authorities, not just acceptable to an investor.

Q6. What is FEMA valuation for AI startups?

When a foreign company acquires an Indian AI startup, or when an Indian AI company receives foreign equity investment, FEMA pricing rules require the share price to be determined by a recognised valuation method (DCF, NAV, or Comparable Company Analysis depending on the instrument). Form FCGPR or FCTRS is filed on the RBI FIRMS portal using this valuation. Incorrect pricing triggers RBI compounding proceedings. Sapient prepares FEMA-compliant AI company valuations certified by IBBI-registered valuers.

Q7. What is ESOP valuation for AI startups and when is it required?

ESOP valuation determines the Fair Market Value (FMV) of shares for option grants, exercises, and buybacks. Under Rule 11UA of the Income Tax Rules, FMV must be determined by a registered merchant banker or IBBI-registered valuer at each grant date. Getting this wrong creates tax exposure for both the company and the employee at the time of exercise. For AI startups with large ESOP pools and frequent grant cycles, an updated valuation every 12–18 months is standard practice.

Q8. What is the Venture Capital Method for AI startup valuation?

The VC Method works backward from a projected exit value — using comparable acquisition multiples or IPO valuations of similar companies — and discounts to the present at a risk-adjusted rate (typically 30–60% for Indian AI startups at early stage). It is most commonly used for pre-revenue or early-revenue AI startups where DCF is impractical. It is also used for ESOP FMV determination and FEMA pricing for early-stage international investment rounds.

Q9. What is Rule 11UA and why does it matter for AI company valuation in India?

Rule 11UA of the Income Tax Rules governs the methodology for determining Fair Market Value of unlisted equity shares in India. It applies to FEMA pricing for cross-border AI company investments, ESOP taxation, and certain M&A transactions. Non-compliance — using an undocumented or incorrect valuation method — creates tax liability for the company and shareholders. AI startups receiving foreign investment or granting ESOPs must ensure valuations are 11UA-compliant.

Q10. How does compute cost affect AI startup gross margin and valuation?

AI inference costs — GPU compute, LLM API calls — sit in cost of goods sold and directly reduce gross margin. An AI company with 80% gross margin is valued materially differently from one with 40% after compute costs. Investors in 2026 explicitly model compute cost as a percentage of revenue and project how it scales. Startups heavily dependent on third-party LLM APIs face the most scrutiny because their compute costs are variable and vendor-controlled.

Q11. What is displacement risk in AI startup valuation?

Displacement risk is the probability that open-source AI models, platform providers (Microsoft, Google, Amazon), or new entrants will commoditise the startup’s core technology — eliminating or severely compressing the competitive moat that justified its valuation premium. IBBI-registered valuers model this as a probability-weighted scenario analysis. Companies with proprietary training data or India-specific language models have lower displacement risk than pure API-wrapper businesses.

Q12. How is an AI startup valuation used in M&A due diligence?

In an M&A transaction, an IBBI-registered business valuation of the AI startup determines the enterprise value and equity value for deal pricing, the share exchange ratio for NCLT merger schemes, the fair value for SEBI open offer purposes if the target is listed, and FEMA pricing for cross-border acquisitions. A non-registered valuation for NCLT scheme filings may face objections at first motion. Sapient provides IBBI-registered valuations for AI company M&A transactions.

Q13. What are the biggest valuation risks for Indian AI startups in 2026?

Three main risks suppress valuations: (1) LLM API dependency — over-reliance on OpenAI, Gemini, or Anthropic APIs that can be repriced or restricted; (2) Government revenue concentration — AI contracts with government clients are valuable but volatile, and investors apply a haircut to government-concentrated ARR; (3) Talent and key-person risk — a small ML engineering team makes the business fragile if key researchers leave.

Q14. Why do Indian AI companies get lower valuations than US AI companies at the same ARR?

Two primary reasons: (1) Market size and pricing power — Indian enterprise clients pay lower SaaS prices than US clients, so ₹1 crore of Indian ARR is worth less to a global investor than $1 million of US ARR at comparable multiples. (2) Liquidity discount — Indian AI startups have fewer credible IPO or acquisition exit pathways than US counterparts, which investors price in via a 20–35% private company discount. International revenue erases most of this gap.

Q15. What does an IBBI-registered valuer provide for an AI startup that a CA or VC does not?

An IBBI-registered valuer provides a documented, methodology-backed, legally defensible valuation report that is accepted by NCLT for merger scheme ratios, SEBI for open offer pricing, RBI for FEMA compliance, income tax authorities for ESOP FMV, and courts in dispute proceedings. A VC term sheet valuation and a CA-prepared valuation are not IBBI-compliant for these specific regulatory filings. Sapient’s valuers are registered under the Securities or Financial Assets (SFA) asset class — the applicable class for AI startup equity.

The Bottom Line — AI Startup Valuation in India in 2026

India’s AI startup valuation environment in 2026 occupies a middle position between Silicon Valley exuberance and the broader Indian startup funding slowdown. Capital is available, investors are active, and the India AI thesis is credible — but the days of raising on a demo and an API wrapper are over.

For founders, AI startup valuation in India in 2026 starts with gross margin quality, burn efficiency, NRR, and a defensible answer to the compute cost question. For investors, the equity valuation analysis requires going beyond ARR multiples to model displacement risk, regulatory revenue concentration, and whether the company’s AI moat is proprietary data or just a positioning claim.

For regulatory, M&A, fundraising, or ESOP purposes — where a documented, IBBI-compliant startup business appraisal is required — Sapient Services provides IBBI-registered valuations with methodology certified for investor, tax authority, and lender scrutiny.

Contact: +91 9540162888 | valuation@sapientservices.com