How to Ensure Accurate Fixed Asset Verification

By

By

Most finance teams assume their asset register is fine — until it isn’t. Fixed assets verification is what separates companies that genuinely know what they own from those who find out the hard way, usually during a statutory audit or an insurance claim.

Machinery moves. Laptops get transferred. Old equipment gets scrapped but nobody updates the books. Furniture shifts floors without a memo. Over years, the gap between what’s recorded and what’s real quietly grows wider.

This article walks through everything you need to conduct accurate fixed asset verification — from cleaning your register before you begin, to handling discrepancies without audit risk. Not theory. Practical, ground-level guidance based on real engagement experience.

What Is Fixed Assets Verification?

Fixed assets verification is the physical inspection and reconciliation of tangible assets listed in a company’s fixed asset register (FAR) against what actually exists on-site. It confirms five things:

- Physical existence — is the asset actually there?

- Location accuracy — is it where the register says it is?

- Condition — does it support the depreciation assumption?

- Identification — do serial/tag numbers match register entries?

- Completeness — have disposed or obsolete assets been removed from books?

Under India’s regulatory framework, this is not optional housekeeping. ICAI’s Guidance Note on CARO 2020 (Para 3(i)) requires statutory auditors to specifically report whether PPE has been physically verified by management at reasonable intervals, and whether any material discrepancies were properly dealt with in the books of account.

That puts the verification responsibility squarely on management — not the auditor. The auditor simply evaluates whether management did it properly.

Related service:

- Fixed Assets Verification Services

- Fixed Assets Componentization Services

- Stock Audit Services in Delhi

Fixed Asset Verification vs. Fixed Asset Audit — What’s the Difference?

These two terms get used interchangeably. They should not be. Here’s a quick comparison:

| Aspect | Fixed Asset Verification | Fixed Asset Audit |

|---|---|---|

| Who does it | Management / outsourced specialist | Statutory / internal auditor |

| Main purpose | Confirm existence, location, condition | Test accuracy of financial reporting |

| Output | Reconciliation report, exception list | Audit findings, qualifications |

| CARO 2020 role | Management’s obligation | Auditor evaluates and reports on it |

| Frequency | Periodic — by risk and asset type | Annual, during statutory audit |

Verification generates the facts. Audit tests whether those facts are reliable. Strong verification makes the statutory audit faster, cheaper, and far less likely to produce a qualified report.

Why Fixed Asset Verification Matters More Than Most Companies Realise

On paper, asset registers look tidy. In practice, even well-managed companies accumulate problems:

- Assets shifted between departments or locations — never updated in the system

- Old machinery scrapped but still on the balance sheet (ghost assets)

- Duplicate asset codes from ERP migrations

- Missing or illegible identification tags

- Capital work-in-progress incorrectly capitalised as active assets

- Fully depreciated assets still in active, productive use

Each of these creates a real-world consequence: depreciation calculations go wrong, insurance coverage becomes unreliable, tax computations get challenged, and balance sheet figures mislead lenders and investors.

Field observation: In one mid-sized manufacturing unit we worked with, nearly 8% of recorded machinery could not be physically located. That unresolved gap directly affected the company’s insurance renewal and statutory audit — problems that could have been avoided with a structured annual verification.

Under Section 128 of the Companies Act, 2013, every company must maintain books of account that give a true and fair view of the state of its affairs — including assets. Inaccurate asset records are a compliance risk, not just an accounting inconvenience.

When Should You Conduct Fixed Asset Verification?

There is no single mandatory cycle — CARO 2020 uses the phrase ‘reasonable intervals’ rather than prescribing a fixed annual requirement. The practical answer: match the frequency to the risk and value of the assets involved.

| Organisation Type | Recommended Frequency | Key Triggers |

|---|---|---|

| Large manufacturing units | Annually | Pre-insurance renewal, statutory audit prep |

| Multi-location corporates | Every 1–2 years | ERP migration, new branch additions |

| Asset-light service companies | Every 2 years | M&A, IPO preparation |

| High-value / high-risk sectors | Annual + surprise checks | Lender requirements, IFC audit |

| Public sector / govt undertakings | As per statutory mandate | CAG audit, government policy directives |

The ICAI’s revised CARO 2020 Guidance Note (2022 edition) makes clear that auditors will evaluate whether the management’s chosen verification interval is actually ‘reasonable’ given the nature, volume, and mobility of assets. Higher-value and higher-risk assets deserve more attention.

Before You Begin: Preparing for Accurate Verification

The quality of your verification is directly tied to the quality of your preparation. Most reconciliation problems are actually preparation failures.

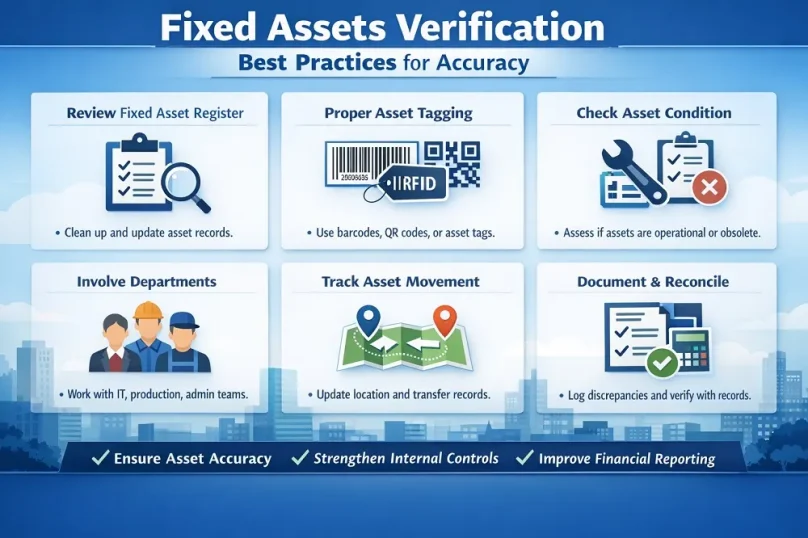

1. Clean the Fixed Asset Register First

Before a single asset is physically checked, review your FAR for:

- Duplicate entries from ERP migrations or manual re-entries

- Incomplete asset descriptions — no make, model, or serial number

- Assets with zero net book value still marked as active

- Capital work-in-progress (CWIP) items that should have been capitalised

- Assets whose useful life was extended without formal documentation

A messy register produces misleading results. Cleaning it first means your verification will surface real discrepancies — not just data-entry noise.

2. Tag Every Asset Before You Start

Asset tagging is one of the highest-return investments a company can make in long-term asset management. The right format depends on the operating environment:

| Tag Type | Best For | Environment |

|---|---|---|

| Barcode labels | Office equipment, IT assets | Standard indoor conditions |

| QR code tags | Multi-data capture, mobile teams | Standard to moderate conditions |

| RFID tags | Large warehouses, manufacturing floors | Works without line-of-sight |

| Engraved / embossed metal plates | Heavy machinery, outdoor assets | Extreme heat, oil, outdoor use |

Tagging creates a reliable, unique identifier that links every physical asset to its register entry. It speeds up future verification cycles and reduces the risk of misidentification during audits.

3. Prepare a Department-Wise Asset List

Do not approach verification randomly. Prepare a department-by-department list and assign specific teams:

- Production and manufacturing floor

- IT, computers, and technology assets

- Administration and corporate offices

- Maintenance and utilities

- Warehouse and logistics

- Company-owned vehicles and fleet

Each department head should formally confirm asset presence and flag anything moved, informally transferred, or returned. This accountability step prevents assets from ‘disappearing’ between verification cycles.

During Verification: What to Check and How to Document It

4. Record Asset Condition, Not Just Existence

Many companies stop at confirming an asset is present. That misses half the point. Condition data directly affects:

- Remaining useful life assessment under Ind AS 16 / AS 10

- Impairment testing under Ind AS 36

- Insurance sum insured accuracy

- Capital budgeting and replacement planning

For each asset, record: working/idle/under-repair status, visible damage or obsolescence, and a rough estimate of remaining life. This turns a compliance exercise into genuinely useful management information.

5. Identify Ghost Assets and Classify All Assets

Ghost assets — assets on the balance sheet that no longer physically exist — inflate reported values, distort depreciation, and can cause insurance claim rejections. Every asset found during verification must be classified:

- Active and in use

- Idle but operational

- Under repair

- Obsolete / beyond economic use

- Missing — requires investigation

This classification drives meaningful capital budgeting decisions and prevents balance sheet misstatement. It also directly satisfies the CARO 2020 requirement to identify and report material discrepancies.

6. Update Location and Custodian Records

For companies with multiple offices or branches, asset shifting is constant. Without documented transfers, your register falls out of date within months.

Every inter-department or inter-location asset movement should have a written transfer memo, an updated custodian record, and formal approval. Without this, audit queries multiply — and so do insurance disputes when a claim involves assets listed at the wrong location.

7. Reconcile With Purchase, Disposal, and Insurance Records

Reconciliation should cross-reference multiple sources — not just compare the physical count to the FAR:

| Document | What It Confirms |

|---|---|

| Purchase invoices | Capitalisation date, original cost, correct classification |

| Disposal / write-off records | Removal of scrapped or sold assets from register |

| Insurance schedules | Coverage accurately reflects the asset base |

| Depreciation schedule | Rates and useful life are still appropriate |

| Transfer memos / approvals | Asset movements between locations are properly recorded |

After Verification: Handling Discrepancies and Updating Records

8. Document Every Discrepancy — Do Not Adjust Silently

Every gap between the register and physical reality must be formally documented. CARO 2020 explicitly requires that material discrepancies are ‘properly dealt with in the books of account’ — and auditors will ask for evidence. Your exception report should include:

- Details of missing assets: last known location, assigned custodian

- Unregistered assets found during inspection

- Estimated financial impact of each discrepancy

- Recommended accounting treatment

- Management sign-off before audit close

Silent adjustments — changing numbers without a documented rationale — are a red flag in both internal control reviews and statutory audits.

9. Follow the Correct Discrepancy Resolution Process

Discrepancies will always emerge. The process matters:

- Investigate — determine when and why the discrepancy arose

- Seek departmental explanation — the custodian usually knows

- Escalate unresolved cases — management sign-off before write-off

- Prepare accounting adjustment memo — document treatment and rationale

- Update the FAR — corrected entry with date and authorisation reference

- Revise depreciation schedule — if asset life or value has changed

- Communicate to auditors — complete transparency reduces audit risk

10. Use Technology to Scale and Speed Up the Process

Manual verification works for small asset bases. Once you have hundreds of assets across multiple sites, technology makes a material difference:

- Handheld barcode or QR scanners for fast, accurate field capture

- Cloud-based reconciliation platforms with real-time dashboards

- ERP integration (SAP, Oracle, Tally) for direct register updates

- GPS tracking for vehicles and mobile equipment

- Digital audit trails with timestamped entries

Technology reduces transcription errors and compresses the time from physical inspection to reconciled report — which matters when audits have tight timelines.

Common Errors Found During Fixed Asset Verification

Based on field experience across manufacturing, corporate, and infrastructure verification engagements, these problems recur most often:

| Common Error | Typical Cause | Practical Impact |

|---|---|---|

| Tag number not matching register | Tag replaced without updating FAR | Misidentification, reconciliation failure |

| Asset under wrong category | Incorrect initial classification | Wrong depreciation rate applied |

| Incorrect capitalisation date | Delay between purchase and commissioning | Depreciation overstated or understated |

| Fully depreciated asset still in active use | No useful-life review after write-down | Asset carrying value understated |

| CWIP treated as active asset | Premature capitalisation | Depreciation on incomplete asset |

| Duplicate asset codes | ERP migration or manual re-entry | Inflated asset base |

Step-by-Step Fixed Asset Verification Process

| Step | Activity | Responsible Party |

|---|---|---|

| 1. Pre-verification prep | Clean FAR, prepare department-wise lists, set up exception format | Finance / Internal Audit |

| 2. Kickoff meeting | Brief department heads, assign teams, confirm timeline | Project Lead |

| 3. Physical inspection | Tag scan or visual check, record condition, note location | Verification Team |

| 4. Reconciliation | Compare physical findings to FAR; log all discrepancies | Finance Team |

| 5. Exception review | Investigate missing/unrecorded assets; gather supporting docs | Internal Audit / Management |

| 6. Accounting adjustments | Write off confirmed missing assets; capitalise found items | Finance / Auditor |

| 7. FAR update | Correct entries with new tags, locations, condition status | Finance Team |

| 8. Final reporting | Issue verification report with findings and recommendations | Finance / Independent Reviewer |

Regulatory Framework: What Indian Companies Must Know

India’s regulatory framework creates specific, documented expectations. These are not suggestions.

CARO 2020 — Companies Auditor’s Report Order

CARO 2020, notified by the Ministry of Corporate Affairs (MCA) on 25 February 2020 and applicable from FY 2021–22, requires statutory auditors to report on three PPE-related matters under Para 3(i):

- Whether the company maintains proper records showing full particulars, including quantitative details and situation of PPE

- Whether PPE has been physically verified by management at reasonable intervals

- Whether material discrepancies noticed on verification were properly dealt with in the books of account

The responsibility to verify sits with management. The auditor’s job is to evaluate whether management has met that responsibility — and to report if they haven’t.

Ind AS 16 / AS 10 — Property, Plant and Equipment

Indian Accounting Standard 16 (Ind AS 16) governs recognition, measurement, and disclosure of PPE for companies following Ind AS. AS 10 governs non-Ind AS companies. Both require that the carrying amount of assets reflects actual economic reality — which physical verification directly supports. An asset that no longer exists cannot have a carrying amount; an asset in deteriorated condition may require impairment.

Companies Act, 2013 — Section 128

Section 128 of the Companies Act, 2013 requires every company to prepare and keep books of account that give a true and fair view of its affairs. Non-compliance can result in penalties including imprisonment up to one year and fines up to Rs 5 lakh for the responsible officers. Accurate asset records are not optional — they are a statutory obligation.

IBC 2016 — Insolvency and Bankruptcy Code

In insolvency resolution proceedings under IBC 2016, verified and documented asset registers are critical for fair valuation. Resolution professionals, creditors, and courts rely on asset data. Independent fixed asset verification is frequently a formal requirement in such proceedings.

- Related service: Valuation for Insolvency and Bankruptcy Code 2016

How Fixed Asset Verification Affects Your Insurance Coverage

Yes — directly. Insurance policies are priced and structured based on the asset data you declare. When that data is out of date, the consequences are real:

- Underinsurance — assets present but not listed means they are effectively uninsured

- Overinsurance — scrapped assets still on the schedule inflate premiums unnecessarily

- Claim rejection — insurer disputes existence or value of an asset at the time of loss

- Incorrect reinstatement value — particularly damaging in fire, flood, or breakdown claims

Periodic verification ensures your insurance schedule reflects current reality. This matters most before policy renewals and in asset-intensive sectors like manufacturing, logistics, and construction.

Fixed Asset Verification in M&A Due Diligence

In mergers and acquisitions, buyers and their advisors price transactions partly on the asset base of the target company. An unverified or inflated register creates direct financial risk:

- Ghost assets inflating the headline asset value

- Hidden obsolescence in machinery or infrastructure

- Unrecorded disposals reducing the real asset base

- Ownership disputes or encumbrances on key assets

Independent pre-acquisition verification gives the buyer a defensible, accurate baseline for pricing and integration planning — and removes the risk of post-transaction disputes based on asset misrepresentation.

Related services:

When Should You Outsource Fixed Asset Verification?

Internal teams can manage routine verification for smaller, single-location organisations. For these situations, independent professional engagement adds clear value:

| Situation | Why Independent Verification Helps |

|---|---|

| Multi-location operations | Consistent methodology and coverage across all sites |

| Large or complex asset base | Specialist scanning technology; structured approach |

| Pre-IPO or fundraising readiness | Third-party credibility for investors and advisors |

| M&A due diligence | Defensible, independent asset baseline for negotiations |

| Lender or bank requirements | Required under loan covenants or credit terms |

| IFC audit gaps or control deficiencies | Documented remediation with audit trail |

| Post-merger asset integration | Reconcile two different registers accurately and efficiently |

Sapient Services provides independent fixed assets verification across India — combining chartered engineering expertise with financial reporting knowledge. Our teams work across manufacturing, corporate, and infrastructure sectors, delivering audit-ready reconciliation reports and documented exception handling.

Contact us: valuation@sapientservices.com | +91 9540162888 | sapientservices.com

Related services: Fixed Assets Verification in Delhi | Fixed Assets Componentization | Stock Audit Services | Impairment Testing of Fixed Assets

Fixed Asset Verification Checklist

Before You Start

- Updated FAR extracted from ERP or accounting system

- Department-wise asset list printed and distributed

- Tagging materials, barcode or QR scanners arranged

- Exception reporting format finalised and shared

- Verification team briefed, areas allocated

During the Verification

- Physical existence of each asset confirmed

- Tag number verified against register entry

- Current location checked against registered location

- Asset condition recorded: active / idle / damaged / obsolete

- Assets with unclear status photographed

- Unregistered assets found on-site flagged and listed

After Verification

- Reconciliation of physical count against FAR completed

- Exception report prepared with all discrepancies documented

- Departmental explanations obtained for missing assets

- Write-offs approved with management sign-off

- Depreciation schedule updated for assets with revised useful life

- Statutory auditors informed of all accounting adjustments

- Final verification report filed with management approval

Fixed Asset Verification and Internal Financial Controls

Under the Internal Financial Control (IFC) requirements in the Companies Act, 2013 — applicable to listed companies and certain unlisted public companies — asset safeguarding is a core control area. Periodic physical verification is a key piece of evidence that your IFC framework is functioning as designed.

Strong verification practices support:

- Prevention of unauthorised asset disposal or misuse

- Detection of internal fraud involving asset manipulation

- Documentation trail for IFC effectiveness reviews

- Auditor satisfaction with management’s control environment

Weak verification, on the other hand, is one of the most common internal control deficiencies raised in IFC reports for asset-heavy companies.

Frequently Asked Questions

1. What is fixed assets verification, and why does it matter?

Fixed assets verification is the process of physically inspecting and reconciling a company’s tangible assets against its fixed asset register. It matters because unverified registers accumulate errors over time — ghost assets, wrong locations, outdated conditions — that distort financial statements and create risk at audit, insurance, and tax time.

2. Is fixed asset verification mandatory under Indian law?

There is no law that specifies a fixed frequency, but CARO 2020 (applicable from FY 2021–22) requires statutory auditors to report whether management has verified PPE at ‘reasonable intervals’ and properly dealt with discrepancies. Under Section 128 of the Companies Act, 2013, companies must maintain accurate books — which makes periodic verification a practical necessity to stay compliant.

3. How often should I physically verify fixed assets?

Annually is the recommended practice for asset-intensive businesses — manufacturing, construction, logistics. Asset-light service companies can typically manage with a two-year cycle. High-value or high-mobility assets should be verified more frequently. CARO 2020’s ‘reasonable intervals’ language means your chosen frequency should match the materiality and movement risk of your specific asset base.

4. What exactly are ghost assets, and how do they harm a company?

Ghost assets are items recorded in the balance sheet that no longer physically exist — scrapped, lost, stolen, or transferred without proper record-keeping. They inflate the reported asset base, overstate depreciation charges, create incorrect insurance coverage, and can trigger audit qualifications. Structured verification is the only way to systematically detect and remove them.

5. What happens if assets go missing during verification?

Missing assets must be formally investigated — not silently written off. The correct process: investigate the reason, get a departmental explanation, obtain management approval, prepare an accounting adjustment memo, update the register, and inform the statutory auditor. CARO 2020 requires that material discrepancies be ‘properly dealt with in the books of account’ — and auditors check for exactly this evidence.

6. My company uses SAP/Oracle — do I still need a physical verification?

Yes, without question. ERP systems only record what humans input into them — and inputs go wrong. The system cannot confirm physical existence, condition, or actual location. Physical verification is the only way to confirm that what your ERP says matches on-the-ground reality. Auditors, insurers, and lenders all ultimately need that physical evidence — ERP data alone does not satisfy them.

7. How does physical verification affect depreciation calculations?

Directly. If an asset is found in worse condition than recorded, the remaining useful life needs revision — which increases future depreciation charges. If an asset is missing or has been scrapped, depreciation on that asset must stop immediately and a write-off recognised. Accurate verification ensures your depreciation schedule reflects actual asset realities, not historical assumptions.

8. What is the right way to tag assets for verification?

The right tagging format depends on the asset and environment. Barcode and QR labels work for most office and IT assets. RFID tags are better for large manufacturing facilities where line-of-sight scanning is impractical. For heavy machinery or outdoor assets in hostile environments, engraved or embossed metal plates are more durable. The goal is a unique, readable identifier on every asset that links it to the register — and lasts long enough to be useful across multiple verification cycles.

9. Does fixed asset verification help during M&A transactions?

It is essential. During M&A due diligence, buyers price transactions partly on the target’s asset base. An independent physical verification confirms what assets genuinely exist, their actual condition, and their realistic value. This prevents overpayment, eliminates post-transaction disputes based on asset misrepresentation, and gives the acquiring team a clean baseline for integration planning.

10. How long does a fixed asset verification exercise take?

It depends on asset volume, number of locations, and how well the register has been maintained. A single-location company with a few hundred assets can typically complete verification in two to three days. A multi-location manufacturing organisation with thousands of assets across sites may need two to four weeks. Engaging a specialist team with barcode or RFID scanning technology can compress timelines significantly compared to manual methods.

Final Thoughts

Fixed assets verification is not about ticking a compliance box. It’s about knowing what you actually own — and making sure your financial statements, insurance policies, and tax filings reflect that reality.

Companies that treat it as a structured, documented, periodic process rarely face balance sheet surprises at audit time, at funding stage, or during a transaction. Those that treat it casually tend to discover their discrepancies at the worst possible moment.

Whether your immediate concern is CARO 2020 compliance, pre-IPO readiness, insurance accuracy, or just cleaning up a register that hasn’t been properly reviewed in years — the path forward is the same: structured verification, proper documentation, and independent review where the stakes are high.

Need help with a verification exercise? Sapient Services delivers independent fixed assets verification, physical asset audits, and FAR reconciliation across India. Contact us: valuation@sapientservices.com | +91 9540162888