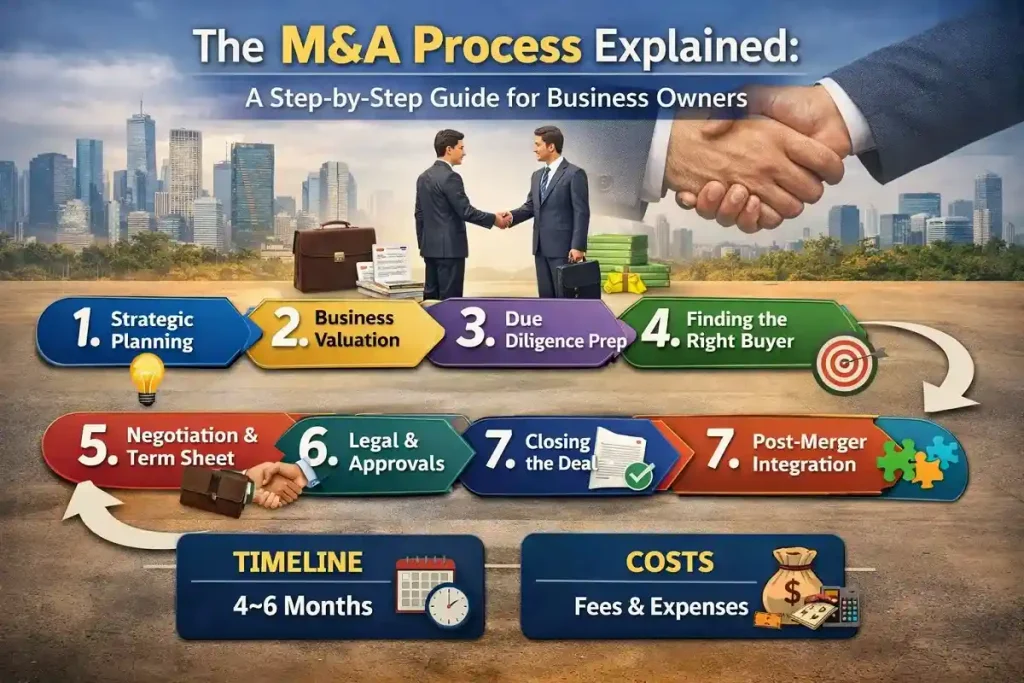

M&A Process Guide for Business Owners

By

By

India has seen consistent deal activity over the past decade across technology, pharma, infrastructure, and manufacturing sectors. Publications like The Economic Times and Business Standard regularly report strong quarterly deal values. What they rarely cover is how many of those transactions quietly fall apart — because preparation was poor or expectations were misaligned from the start.

This guide walks through the M&A process as it actually happens for Indian promoters — and how Mergers & Acquisitions Advisory Services in India can help you navigate each stage more effectively, from preparation to closing.

Step 1: Know What You Actually Want

Before approaching any buyer, a promoter needs honest internal clarity on one question: what outcome am I personally willing to accept?

This sounds obvious but it isn’t. In one mid-sized engineering business, the promoters told buyers the deal was a ‘strategic partnership’ — internally, they wanted majority liquidity. The confusion stretched negotiations by nearly two months and nearly killed the deal. Clarity on this upfront is not about strategy. It is about not wasting everyone’s time, including your own.

Common reasons promoters enter M&A include the need for expansion capital, investor exit pressure, succession issues (such as no clear second-generation interest), or competitive dynamics that make a deal necessary. Understanding the primary driver helps shape your negotiation strategy and determine which terms to prioritise.

Step 2: Get the Business Ready Before You Go to Market

Most deals that underperform on valuation do so because problems surface during due diligence that the seller did not address beforehand. A buyer who finds three compliance gaps and two years of unaudited financials will price that risk into their offer — or walk.

What readiness actually looks like:

- Financials: 3 years of audited statements. EBITDA normalised — owner salaries above market rate, personal expenses, one-time items removed. Clear working capital picture.

- Legal: Title clear on all key assets. Shareholder agreements updated. No undisclosed litigation pending.

- Tax: GST returns filed, no open scrutiny orders, no pending income tax demands.

- Operations: The business should be able to function without the promoter in the room. Key employees have retention agreements. Processes are documented.

- Data room: A virtual data room with all of the above — organised, categorised, ready for a buyer’s team to access without chasing you for documents every week.

Six months of preparation before market entry is realistic. Less than three months is usually not enough.

Suggested to Read:

Step 3: Valuation — What Buyers Actually Pay and Why

Founders value a business based on what they put into it. Buyers value it based on what they expect to get out. The gap between those two views is what negotiations are about.

In Indian mid-market transactions — roughly ₹50 crore to ₹500 crore in revenue — EBITDA multiples are the standard reference. Manufacturing businesses typically trade at 4x–6x EBITDA. Technology and healthcare businesses with recurring revenue can reach 6x–10x. These are ranges, not guarantees. The actual multiple a buyer offers depends on how much risk they see.

Risk shows up in three places: customer concentration (one customer above 30% of revenue is a discount), management dependency (a business that cannot run without the founder gets a lower multiple), and documentation quality (unaudited numbers, pending tax demands, unresolved litigation — each one adds to the escrow demand or reduces the headline price). Getting those three things right before going to market is how you protect your valuation.

Step 4: Finding the Right Buyer

There are broadly three types of buyers in the Indian market: strategic buyers, private equity funds, and family offices.

Strategic buyers — a competitor, a customer, or a company in an adjacent sector — typically pay more when they see synergy. They are acquiring your customers, technology, or market position as much as your earnings. PE funds are buying cash flow and a management team they can back. They are financial buyers with return targets and a defined exit horizon (usually 4–7 years). Family offices are often longer-term holders and more flexible on structure.

The buyer type affects what you give up. A strategic buyer may want to merge operations — your brand or team may not survive in its current form. A PE fund will push for governance rights, board representation, and an eventual secondary exit. Knowing this before you start talking to buyers changes how you negotiate.

Confidentiality matters throughout. A leak before deal certainty unsettles employees, can affect customer relationships, and sometimes triggers competitor action.

Step 5: Term Sheet

When a buyer is serious, they issue a Non-Binding Offer or term sheet. It covers the headline valuation, deal structure, payment split (upfront vs. deferred), exclusivity period, and any key conditions.

Two clauses trip up promoters most often. First, the working capital adjustment — if the business’s working capital at closing is different from the agreed benchmark, the final payment changes. This is not a small rounding issue. On a ₹100 crore deal, a 10% working capital shortfall can reduce the consideration by ₹10 crore.

Second, earn-outs. When the buyer and seller cannot agree on a valuation based on current numbers, the buyer often proposes paying part of the price based on future performance. The concept is reasonable. The problem is execution — earn-out disputes are common in India and usually come down to ambiguous metric definitions or the buyer making post-close decisions that affect the seller’s ability to hit the targets. Before accepting an earn-out, read the drafting carefully.

Step 6: Due Diligence

Due diligence is the buyer’s right to verify everything you represented in the sale process. It covers financial statements, tax filings, legal documents, contracts, licences, and key employee arrangements. A serious buyer’s DD team will ask for a lot. How quickly and completely you respond affects both the timeline and the buyer’s confidence.

A well-prepared data room — audited financials, 3 years of tax returns, key contracts, IP registrations, regulatory licences, litigation disclosures — makes this process faster and cleaner. Every gap the buyer finds in the data room is a reason to slow down, ask more questions, or adjust the price. Sellers who have done the preparation in Step 2 move through due diligence significantly faster.

Step 7: Definitive Agreements

The lawyers take over here. The Share Purchase Agreement (SPA) and Shareholders’ Agreement (SHA) formalise every commercial term that was agreed verbally or in the term sheet. Every clause around representations, warranties, indemnities, and risk allocation gets drafted and negotiated.

One question that comes up at this stage — and should come up earlier — is whether the deal is structured as a share sale or an asset sale. In a share sale, the buyer acquires the company as a whole, including all liabilities known and unknown. In an asset sale, specific assets transfer and most liabilities stay with the seller. The tax treatment for a promoter is different under both: share sales are typically taxed as capital gains; asset sales depend on the asset class. Discuss this with your CA well before you reach the SPA stage.

Step 8: Regulatory Approvals and Closing

Most mid-market transactions do not require Competition Commission of India (CCI) approval. CCI filing is mandatory only when combined Indian assets of both parties exceed ₹2,000 crore or combined Indian turnover exceeds ₹6,000 crore. If either party is foreign, separate worldwide thresholds apply.

Sector-specific approvals are a different matter. NBFC acquisitions require RBI approval. Acquisitions of listed companies require SEBI open offer compliance. Insurance sector deals need IRDA clearance. Map these out at the start — not two weeks before expected closing.

Closing is the mechanics: fund transfer, share transfer, board changes, and statutory filings with the Registrar of Companies. It sounds simple but the documentation is detailed. Most deals have a signing date and a separate closing date, with conditions that must be satisfied in between.

Step 9: After the Deal Closes

A deal that closes well can still fail to deliver. Integration is where value is created or destroyed after the transaction.

Three areas consistently cause problems in Indian mid-market deals post-closing:

- Key people: Employees who were not part of the deal announcement often feel uncertain about their roles, reporting lines, and pay. The ones who leave first are usually the ones you most need. Retention decisions and communication should be finalised before closing, not made up on day one.

- Finance and systems: Aligning MIS, accounting policies, and compliance reporting between the acquired company and the buyer takes months. Both sides underestimate this consistently.

- Customers and vendors: A change of ownership is a trigger for contract reviews, renegotiations, or exits for key customers and suppliers. The outgoing promoter usually needs to stay visible and communicative during the transition — a cold handover rarely works.

If there is an earn-out, post-close integration is more complicated. The seller has a financial interest in how the business is run, but the buyer has operational control. Disputes about accounting decisions, allocation of shared costs, and investment decisions are common. The SPA needs to address these scenarios specifically.

How Sapient Services Works with Promoters Through This Process

Sapient Services works with business owners at each stage — from preparing the business before market entry to supporting transaction advisory and regulatory compliance:

- Financial preparation: EBITDA normalisation, working capital review, financial data room organisation

- Valuation advisory: Sector-benchmarked valuation range before buyer conversations begin

- Due diligence readiness: Data room preparation, compliance gap identification

- Transaction support: Term sheet review, SPA input, deal structuring

- Regulatory: CCI threshold analysis, SEBI and RBI requirements where applicable

The focus is on reducing uncertainty before it affects valuation.

Frequently Asked Questions

Q-1: How long does an M&A transaction take?

Most mid-market deals in India take 6–9 months from the time you engage an advisor to when the money transfers. Straightforward deals with clean financials can close in 4–5 months. Complex situations — multiple regulatory approvals, valuation disagreements, messy cap tables — can take 12–18 months. The 4–6 month estimates you see in presentations assume everything is ready when the process starts. It usually isn’t.

Q-2: Can valuation change after the term sheet?

Yes. Due diligence is the most common trigger — an undisclosed liability, a concentrated customer base, or financial irregularities found by the buyer’s team typically result in a price chip or additional escrow. Working capital adjustments at closing also affect the final number. The term sheet is not the final price.

Q-3: What is an earn-out?

Part of the sale consideration is paid later, based on whether the business hits agreed targets — usually revenue or EBITDA — after the deal closes. It bridges a valuation gap between buyer and seller. The risk for the seller is that post-close operational decisions made by the buyer can make those targets harder to hit. Earn-out drafting in the SPA needs to be specific about who controls what.

Q-4: Does every M&A deal need CCI approval?

No. CCI approval applies only when the combined Indian assets cross ₹2,000 crore or combined Indian turnover crosses ₹6,000 crore. Most mid-market Indian deals are well below these numbers and need no CCI filing. Sector regulators — RBI, SEBI, IRDA — have separate and independent requirements that may still apply.

Q-5: What is escrow in an M&A deal?

A portion of the purchase price — typically 10–15% — is held by a neutral third party after closing. The buyer can make claims against it if the seller’s representations turn out to be inaccurate. If there are no claims within the agreed period (usually 12–24 months), the amount goes to the seller. It is standard practice in most structured transactions.

Q-6: Can I sell only a minority stake?

Yes. PE funds frequently take 25–49% stakes, leaving the promoter in control and continuing to run the business. The governance rights — board seats, veto rights, drag-along and tag-along provisions — attached to that minority position are what matter and need careful negotiation in the SHA.

Q-7: Why do deals fall apart late in the process?

The most common reasons: due diligence uncovers something the seller did not disclose and cannot adequately indemnify; a valuation gap resurfaces in SPA drafting that the term sheet had papered over; a key employee or the promoter signals they are leaving post-deal; or a regulatory approval takes longer than expected. Late-stage failures are expensive for everyone.

Q-8: When should employees be told about the deal?

After deal certainty is high — typically post-signing, before closing. Telling employees too early creates anxiety, sometimes resignations, and occasionally customer concern. Telling them too late creates resentment. The communication plan should be part of the deal playbook, not an afterthought.

Q-9: What drives valuation most?

Quality of earnings — meaning how consistent, audited, and clean the EBITDA is. Customer concentration is the second biggest factor. A single customer above 25–30% of revenue compresses the multiple noticeably. After that: management depth (can the business run without you?), and compliance cleanliness (unresolved tax or legal matters create either price reductions or escrow demands).

Q-10: When should I bring in an advisor?

Before you start talking to buyers. An advisor sets a realistic valuation range, manages confidentiality during the buyer approach, and gives you negotiating discipline at each stage. Coming in after a buyer has already approached you means starting at a disadvantage — they have had time to think about the deal; you haven’t.

The M&A process demands preparation, patience, and realism. It is not just a financial transaction — it is a strategic turning point. When approached thoughtfully, it unlocks capital, scale, and long-term value.