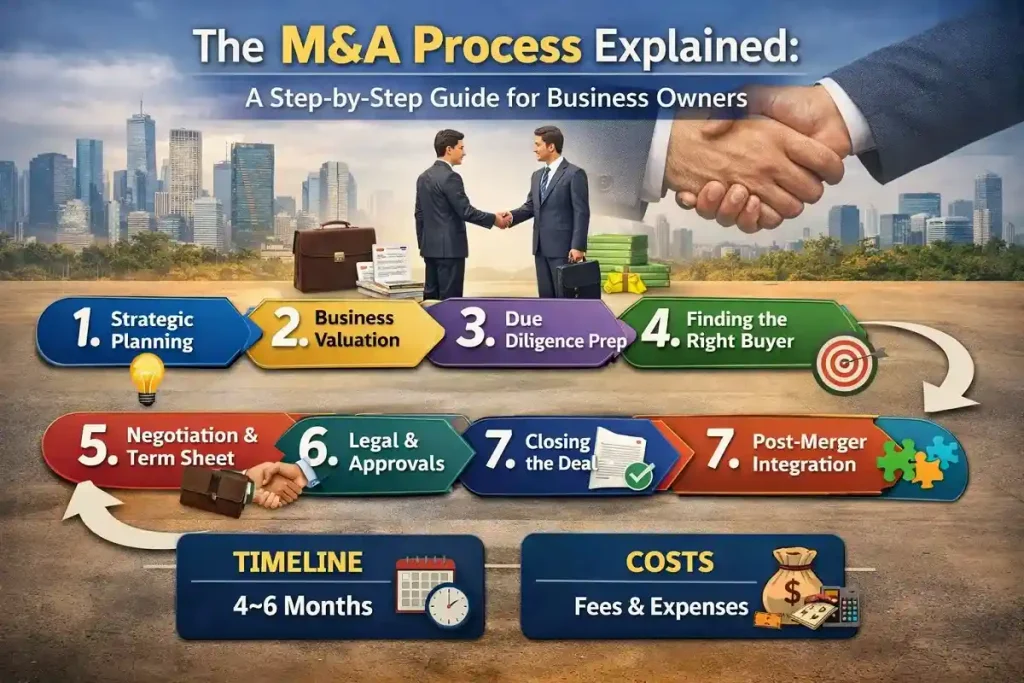

M&A Process Guide for Business Owners

By

By

When business owners hear about mergers and acquisitions, it usually comes wrapped in headlines — “strategic acquisition,” “successful exit,” “multi-crore deal.” It sounds smooth, almost celebratory.

But if you’ve ever sat across a table negotiating your own company’s sale or acquisition, you know the reality is far more layered. The M&A process is not a straight road. It stretches, pauses, circles back, and sometimes tests patience more than expected.

India has seen consistent deal activity over the past decade across technology, pharma, infrastructure, and manufacturing sectors. Publications like The Economic Times and Business Standard regularly report strong quarterly deal values. What they don’t highlight enough is how many transactions quietly fall apart because preparation was weak or expectations were unrealistic.

This guide explains the M&A process and advisory services in practical terms — the way transactions actually unfold for promoters, not the way they appear in PowerPoint decks.

What Is the M&A Process in Practical Terms?

The M&A journey refers to the structured path through which a company is sold, merged, or partially acquired by another entity. On paper, it appears linear. In practice, it’s iterative. Negotiations reopen. Valuations shift. Risk discussions intensify.

In India, corporate transactions are governed primarily under the Companies Act 2013. Listed entities must also follow regulations issued by the Securities and Exchange Board of India. If deal size crosses certain thresholds, approval from the Competition Commission of India may be mandatory.

But compliance is just one layer. The deeper challenges usually involve:

- Aligning promoter expectations

- Presenting clean financial records

- Managing tax exposures

- Structuring working capital adjustments

- Handling employee communication

If these areas aren’t organized early, the transaction slows down later — sometimes critically.

Step 1: Strategic Clarity Before Entering the M&A Process

Before valuation discussions even begin, founders need internal clarity. Why exactly are you entering this transaction?

Common triggers include expansion funding, investor exit pressure, succession planning, or competitive positioning. But beneath that surface reason lies a more important question — what outcome are you personally comfortable with?

Ask yourself:

- Do I want a complete exit or partial dilution?

- Am I ready to report to a board I don’t fully control?

- Is liquidity my primary goal, or long-term partnership?

- What is my minimum acceptable valuation threshold?

In one mid-sized engineering business, promoters publicly positioned the deal as a strategic partnership. Privately, they wanted majority liquidity. That misalignment confused buyers and prolonged negotiations for nearly two months.

Clarity at this stage shortens timelines and strengthens negotiating confidence.

Step 2: Valuation – Where Emotion Meets Market Reality

Valuation is often the most sensitive part of any transaction. Founders see brand equity, relationships, and years of sweat. Buyers evaluate cash flow stability, risk exposure, and scalability.

In Indian mid-market transactions, EBITDA multiples are widely used. Sector trends covered by The Hindu BusinessLine frequently highlight this benchmark approach. However, multiples are not fixed numbers. They reflect confidence.

Buyers quietly examine:

- Customer concentration ratios

- Pending litigation

- Tax compliance history

- Sustainability of margins

- Dependence on promoter relationships

Common Valuation Approaches

| Method | Best Suited For | Ground Reality |

|---|---|---|

| EBITDA Multiple | Profitable firms | Most common benchmark |

| DCF Model | Growth companies | Sensitive to assumptions |

| Comparable Deals | Active sectors | Depends on recent data |

| Asset-Based | Manufacturing/infra | Sets floor value |

Uncertainty reduces multiples faster than low profit does. Clean documentation increases bargaining power.

Step 3: Preparing for Due Diligence (Before It Begins)

Many business owners underestimate this phase. Due diligence is not a formality — it is a forensic review.

Buyers typically request:

- Three years audited financials

- GST and income tax filings

- Vendor and customer agreements

- Employee contracts

- Intellectual property documentation

- Litigation disclosures

Deal coverage in Mint has repeatedly noted that undisclosed liabilities often lead to valuation adjustments.

In a recent advisory observation, a logistics company faced a 10–15% valuation revision due to unresolved indirect tax reconciliations. The issue was solvable — but it surfaced too late.

Preparation ahead of market approach protects value and avoids renegotiation fatigue.

Step 4: Buyer Identification and Confidential Outreach

Not every buyer is right for your business. Some bring synergy. Others bring capital discipline.

Typically, buyers fall into:

- Strategic acquirers

- Private equity funds

- Family offices

Each category has different expectations around governance, control, and growth acceleration.

The outreach sequence usually looks like this:

- NDA execution

- Teaser circulation

- Information Memorandum sharing

- Management meetings

Confidentiality during this phase is critical. Premature information leaks can unsettle employees or customers.

Step 5: Negotiation and Term Sheet Dynamics

Once a buyer shows serious intent, a Non-Binding Offer or term sheet is issued. This outlines valuation, deal structure, payment terms, and exclusivity period.

Important negotiation areas include:

- Working capital adjustments

- Escrow percentage

- Indemnity caps

- Earn-out structures

- Non-compete duration

Working capital adjustments often surprise promoters. If actual working capital at closing differs from the benchmark, the final consideration changes.

Small clause. Significant impact.

Step 6: Documentation and Regulatory Approvals

After commercial alignment, lawyers draft definitive agreements such as the Share Purchase Agreement (SPA) and Shareholders’ Agreement (SHA). Every clause — especially around risk allocation — is negotiated carefully.

If thresholds are crossed, regulatory approval from the Competition Commission of India becomes necessary. Sector regulators may also step in depending on industry.

Documentation is detailed and time-consuming because risk transfer is being formalized.

Step 7: Closing and Integration

Closing includes fund transfer, share transfer, board restructuring, and statutory filings. Coordination between financial institutions and advisors becomes crucial here.

However, the real work begins post-closing.

Integration typically covers:

- IT system harmonization

- HR restructuring

- Vendor consolidation

- Brand strategy alignment

Cultural mismatch is one of the most common post-merger challenges globally.

Typical Timeline of a Mid-Market Transaction in India

| Stage | Approx Duration |

|---|---|

| Preparation | 4–6 weeks |

| Outreach | 6–8 weeks |

| Negotiation | 3–4 weeks |

| Due Diligence | 6–10 weeks |

| Documentation & Closing | 4–6 weeks |

Overall duration: roughly 4–6 months, depending on complexity.

Cost Structure Overview

| Component | Estimated Range |

|---|---|

| Investment Banker | 1–3% of deal value |

| Legal Fees | ₹15–50 lakh+ |

| Financial Due Diligence | ₹10–30 lakh |

| Valuation Advisory | ₹5–15 lakh |

Costs vary based on transaction scale and sector.

Common Mistakes Business Owners Make

- Entering market without compliance cleanup

- Overstating projections

- Ignoring tax structuring

- Negotiating emotionally

- Delaying professional advisory support

Prepared businesses negotiate from strength.

How Sapient Services Supports Business Owners

Sapient Services works closely with promoters to prepare businesses before entering discussions. Support areas include:

- Independent valuation

- Financial restructuring analysis

- Due diligence readiness

- Risk assessment

- Transaction structuring

The focus remains on reducing uncertainty before it reduces valuation.

FAQs

Q-1: How long does a typical transaction take?

Ans: Around four to six months for mid-sized businesses.

Q-2: Can valuation change after term sheet?

Ans: Yes, especially after due diligence findings.

Q-3: What is an earn-out structure?

Ans: A portion of payment linked to future performance.

Q-4: Do all deals require CCI approval?

Ans: Only if asset/turnover thresholds are crossed.

Q-5: What is escrow?

Ans: Temporary holding of funds for risk coverage.

Q-6: Can I sell only minority stake?

Ans: Yes, structured dilution is common.

Q-7: Why do deals fail late?

Ans: Compliance or governance disagreements.

Q-8: Should employees be informed early?

Ans: Usually after deal certainty improves.

Q-9: What affects valuation most?

Ans: Risk clarity and documentation quality.

Q-10: When should advisors be appointed?

Ans: Ideally before buyer outreach begins.

The M&A process demands preparation, patience, and realism. It is not just a financial transaction — it is a strategic turning point. When approached thoughtfully, it unlocks capital, scale, and long-term value. When rushed, it becomes exhausting and uncertain.